Atal Pension Yojana in India Explained: Pension Benefits, Contribution & Eligibility (2026 Guide)

Atal Pension Yojana in India Explained: Simple Guide for Guaranteed Retirement Pension

Atal Pension Yojana in India Explained: Pension Benefits, Contribution & Eligibility (2026 Guide)

Learn how Atal Pension Yojana (APY) works in India with simple examples. Understand pension amounts, contribution chart, eligibility, tax benefits, and retirement planning.

Atal Pension Yojana APY passbook India savings example

Atal Pension Yojana enrollment form bank branch India

APY pension contribution chart age wise India infographic

Indian worker checking Atal Pension Yojana balance mobile app

Atal Pension Yojana account opening process India bank

For many Indian citizens—daily wage workers, shopkeepers, drivers, helpers, and small business owners—retirement planning feels like a luxury.

Most people think:

“I will work as long as I can.”

“Who will support me after 60?”

“I don’t have EPF or pension.”

To solve this problem, the government introduced a simple scheme:

👉 Atal Pension Yojana (APY)

In this article, we will explain Atal Pension Yojana in India in a simple, practical, and friendly way, using real Indian examples.

No complex pension language. Only clear understanding.

What Is Atal Pension Yojana? (In Simple Words)

Atal Pension Yojana (APY) is a government-backed pension scheme.

Its purpose is:

✅ Give fixed monthly pension after 60

✅ Support unorganized workers

✅ Encourage long-term savings

✅ Reduce old-age dependency

In short:

👉 APY = Guaranteed pension for common Indians

It is regulated by:

👉 Pension Fund Regulatory and Development Authority (PFRDA)

Who Can Join Atal Pension Yojana?

You can open APY account if:

✅ Age is between 18 and 40 years

✅ You have a savings bank account

✅ You are an Indian citizen

Best suited for:

Drivers

Vendors

Farmers

Domestic workers

Small shop owners

Self-employed people

People without EPF/NPS benefit most.

Main Features of APY

| Feature | Details |

|---|---|

| Scheme Type | Government Pension |

| Entry Age | 18–40 Years |

| Pension Age | 60 Years |

| Pension Amount | ₹1k to ₹5k per month |

| Contribution Period | Till 60 |

| Risk | Very Low |

| Guarantee | Yes |

| Nominee Benefit | Yes |

APY gives fixed pension for life.

Pension Options Under APY

You can choose how much pension you want after 60.

| Monthly Pension | Who Should Choose |

|---|---|

| ₹1,000 | Very low income |

| ₹2,000 | Small traders |

| ₹3,000 | Self-employed |

| ₹4,000 | Stable earners |

| ₹5,000 | Young earners |

Higher pension = Higher contribution.

How APY Works (Step-by-Step)

Let’s understand simply.

Step 1: Open APY Account

Visit your bank branch and apply.

Your bank links APY to your savings account.

Step 2: Choose Pension Amount

Select ₹1k–₹5k pension.

Bank calculates monthly contribution.

Step 3: Monthly Auto-Debit

Money is automatically deducted every month.

No need to remember.

Step 4: Continue Till 60

You keep contributing till age 60.

Step 5: Get Pension

After 60:

👉 Monthly pension starts for life.

After your death, spouse gets pension.

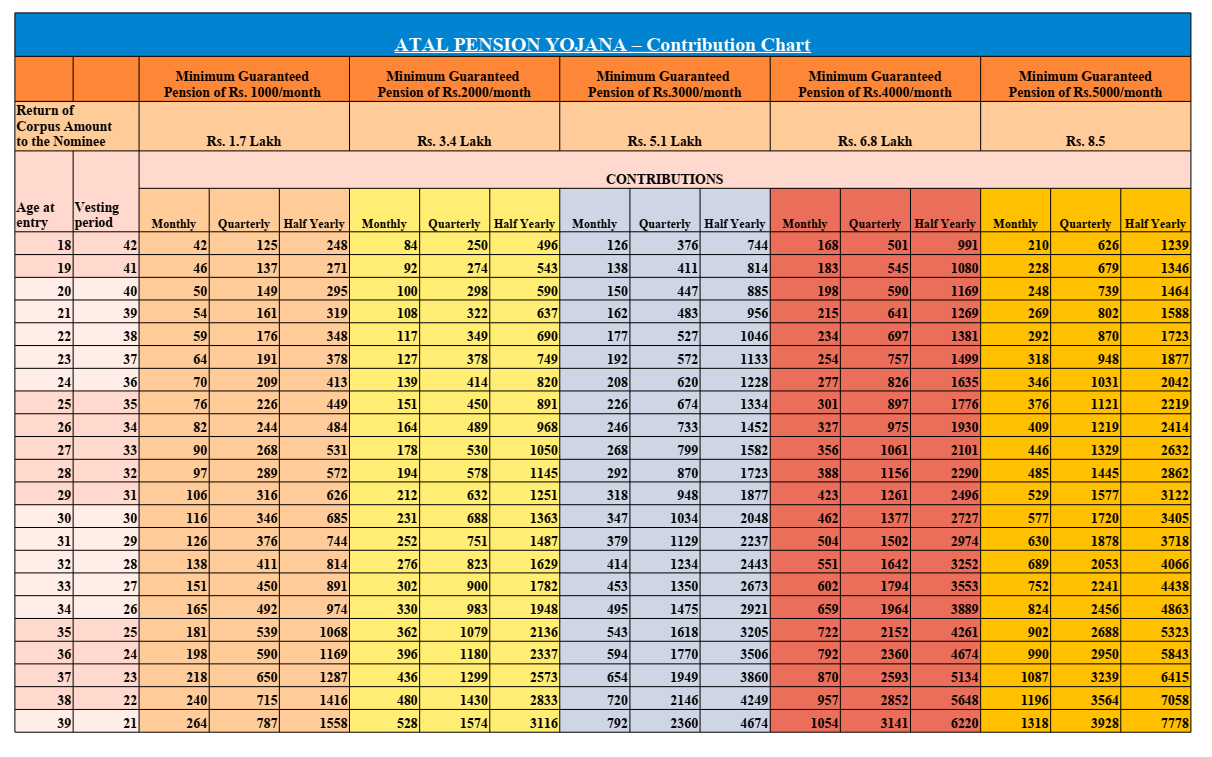

Contribution Chart (Simple Example)

Contribution depends on:

Your age

Chosen pension

Example: ₹5,000 Pension Plan

| Entry Age | Monthly Contribution |

|---|---|

| 20 Years | ₹210 approx |

| 25 Years | ₹315 approx |

| 30 Years | ₹577 approx |

| 35 Years | ₹902 approx |

| 40 Years | ₹1,454 approx |

Earlier you join = Less you pay.

Chart: APY Working Flow

Open Account (18–40)

↓

Monthly Contribution

↓

Auto Debit

↓

Continue Till 60

↓

Lifetime Pension

Simple and systematic.

Calculation Example: Real Indian Case

Case: Raju (Auto Driver, Indore)

Age: 25

Chosen Pension: ₹3,000

Monthly Contribution: ₹181 (approx)

Contribution Period: 35 years

Total Contribution:

₹181 × 12 × 35 ≈ ₹76,000

After 60:

👉 Gets ₹3,000/month = ₹36,000/year

For life.

Raju invests little, gets lifelong income.

Case: Sunita (Tailor, Patna)

Age: 35

Pension: ₹5,000

Contribution: ₹902/month

After 60:

👉 ₹5,000 every month

Helps in medicines and bills.

APY vs NPS vs PPF

| Feature | APY | NPS | PPF |

|---|---|---|---|

| Pension | Fixed | Market-based | No |

| Risk | Very Low | Medium | Very Low |

| Entry Age | 18–40 | 18–70 | All |

| Lock-in | Till 60 | Till 60 | 15 Years |

| Suitable For | Informal Workers | Salaried/Self | All |

👉 APY = Guarantee

👉 NPS = Growth

👉 PPF = Safety

👉 Related Read:

Internal Link: NPS Scheme in India Explained

https://marketmeterab.blogspot.com/nps-scheme-india

Government Co-Contribution (Earlier Benefit)

Earlier, government contributed for some subscribers (2015–2019). Now, new accounts do not get this.

Still, APY remains very useful.

Tax Benefits in APY

APY qualifies under:

👉 Section 80CCD (part of 80C limit)

Benefit:

Contribution up to ₹1.5 lakh is deductible

Pension received is taxable as per slab.

👉 Related Read:

Internal Link: Mutual Fund Taxation in India

https://marketmeterab.blogspot.com/mutual-fund-taxation-india

Withdrawal Rules in APY

After 60 (Normal Exit)

Full pension starts

Before 60 (Exit)

Allowed only in:

Death

Serious illness

Otherwise, exit is discouraged.

APY is meant for long-term discipline.

Nomination and Family Benefit

APY protects family.

If subscriber dies:

✔ Spouse gets pension

✔ After spouse, nominee gets corpus

Always update nominee details.

Who Should Choose APY?

APY is best for:

✅ Low-income workers

✅ Informal sector employees

✅ People without EPF/NPS

✅ Risk-averse citizens

✅ Young earners

Not ideal for:

❌ High-income professionals

❌ Investors seeking high returns

Best Strategy for Common Indians

Smart planning:

| Tool | Purpose |

|---|---|

| APY | Guaranteed Pension |

| PPF | Safety |

| SIP | Growth |

Example:

APY: ₹300/month

SIP: ₹2,000/month

PPF: ₹30,000/year

Balanced future.

👉 Related Read:

Internal Link: Long Term vs Short Term Investing

https://marketmeterab.blogspot.com/long-term-vs-short-term-investing

How to Open APY Account

You can open APY in:

✅ Any nationalized bank

✅ Private banks

✅ Regional rural banks

Documents Required

Aadhaar

Mobile number

Bank passbook

Steps

1️⃣ Visit bank

2️⃣ Fill APY form

3️⃣ Choose pension

4️⃣ Submit documents

5️⃣ Activate auto-debit

Takes 15–30 minutes.

Common Mistakes Indians Make in APY

Joining late (after 35)

Missing balance in bank

Choosing very low pension

Not updating nominee

Stopping contributions

Avoid these.

Safety of Atal Pension Yojana

APY is backed by Government of India.

So:

✔ No market risk

✔ No company risk

✔ No default risk

It is among the safest pension schemes.

Role of Market Regulator

While APY is regulated by PFRDA, market investments are supervised by:

👉 Securities and Exchange Board of India

So, overall investor system is protected.

Statutory Disclaimer

Atal Pension Yojana rules, pension amounts, and tax benefits are subject to change as per Government of India and PFRDA guidelines. This article is for educational purposes only and does not constitute financial advice. Investors should assess their financial needs and consult a qualified advisor before joining any scheme.

Frequently Asked Questions (FAQ)

Q1. Is APY guaranteed?

Yes. Pension amount is guaranteed.

Q2. Can I change pension amount later?

Yes, once in a year (subject to rules).

Q3. Is APY better than NPS?

For guarantee, yes. For growth, NPS is better.

Q4. Can salaried people join APY?

Yes, if eligible by age and not covered by statutory pension.

Q5. What if I miss payment?

Penalty is charged. Keep bank balance.

Useful Video & Image Resources

APY Explained in Hindi:

https://www.youtube.com/watch?v=F8M2Q9L7X4AAtal Pension Yojana Guide:

https://www.youtube.com/watch?v=K9F3L2M8X7Q

Bibliography

PFRDA Annual Reports

Ministry of Finance Notifications

APY Scheme Guidelines

Income Tax Act – Section 80CCD

RBI Financial Stability Reports

Suggested Internal Links for MarketMeterAB

Senior Citizen Saving Scheme Explained

https://marketmeterab.blogspot.com/senior-citizen-saving-schemeEPF vs PPF Difference Explained

https://marketmeterab.blogspot.com/epf-vs-ppf-differenceNPS Scheme in India Explained

https://marketmeterab.blogspot.com/nps-scheme-indiaPPF in India Explained

https://marketmeterab.blogspot.com/ppf-india-explainedHow Dividends Work in India

https://marketmeterab.blogspot.com/how-dividends-work

Final Words

Atal Pension Yojana is not about big money.

It is about:

✅ Dignity in old age

✅ Regular income

✅ Independence

✅ Peace of mind

If you or someone in your family works in the informal sector, APY is a gift.

👉 Remember: A small saving today can protect your tomorrow. Start early. Stay regular.

Comments

Post a Comment