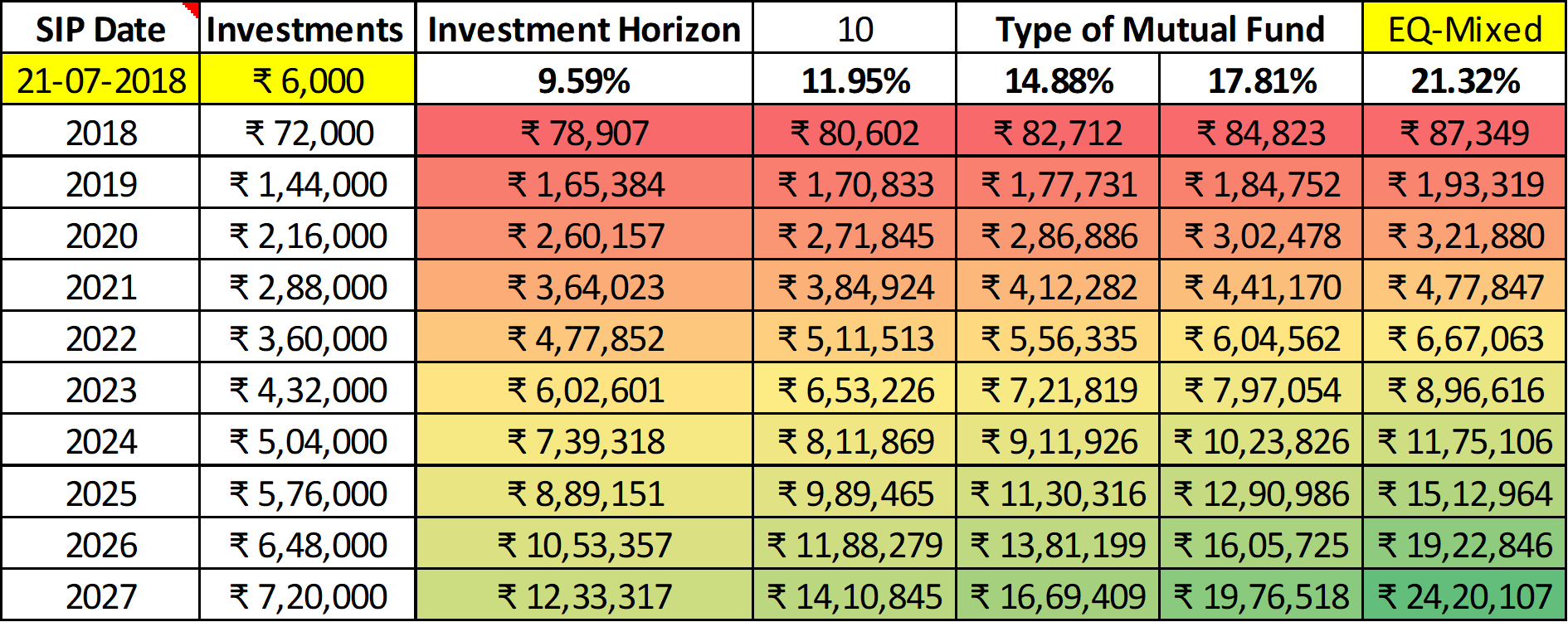

Best SIP Amount for Beginners in India (Simple & Practical Guide)

Best SIP Amount for Beginners in India (Simple & Practical Guide)

If you are an Indian working adult or middle-class family person, you already know one thing clearly — saving money is necessary, but growing money is even more important. This is where SIP (Systematic Investment Plan) becomes a powerful yet simple tool.

But beginners usually ask one confusing question:

“What is the best SIP amount to start with in India?”

There is no single fixed answer. The right SIP amount depends on your income, lifestyle, responsibilities, and goals. This article explains everything in a clear, practical, and realistic Indian context, without heavy financial words.

What is SIP in Simple Words?

SIP means investing a fixed amount every month in a mutual fund.

Example:

You invest ₹2,000 every month

The money goes into a mutual fund

Over time, your money grows through compounding

You don’t need to time the market. SIP works like a monthly habit, just like paying your mobile bill.

👉 If you are completely new, first read:

Internal Link: What is SIP and How SIP Works in India

https://marketmeterab.blogspot.com/what-is-sip-india

Why SIP is Best for Beginners in India?

For Indian beginners, SIP is ideal because:

No large lump sum needed

Can start with very small amount

Works well with monthly salary

Reduces market risk over time

Easy to stop or modify anytime

Even tea sellers, delivery executives, office staff, and teachers can start SIP.

Best SIP Amount for Beginners in India (Realistic Numbers)

Let’s break this into practical income-based slabs.

1. If Monthly Income is ₹15,000 – ₹25,000

Recommended SIP amount:

👉 ₹500 – ₹1,000 per month

Reason:

Focus on habit, not amount

Emergency fund is priority

Lower pressure on monthly budget

Example:

₹1,000/month for 20 years

Estimated value (12% return): ₹9–10 lakh

2. If Monthly Income is ₹25,000 – ₹40,000

Recommended SIP amount:

👉 ₹2,000 – ₹3,000 per month

Reason:

Stable income

Some savings after expenses

Can take small market risk

Example:

₹3,000/month for 20 years

Estimated value: ₹27–30 lakh

3. If Monthly Income is ₹40,000 – ₹60,000

Recommended SIP amount:

👉 ₹4,000 – ₹6,000 per month

Reason:

Better cash flow

Can plan long-term goals

Suitable for wealth creation

Example:

₹5,000/month for 20 years

Estimated value: ₹45–50 lakh

4. If Monthly Income Above ₹60,000

Recommended SIP amount:

👉 10–20% of monthly income

Example:

Income: ₹80,000

SIP: ₹8,000 – ₹15,000

Long-term corpus can cross ₹1 crore with discipline

Golden Rule for Beginners (Very Important)

👉 Start small, increase slowly.

Do not start with a high SIP and then stop after 6 months.

A ₹1,000 SIP continued for 20 years is better than ₹10,000 SIP stopped in 1 year.

Ideal SIP Allocation for Beginners (Simple Table)

| Goal Type | SIP Percentage |

|---|---|

| Emergency / Short Term | 0% (use savings/FD) |

| Wealth Creation (Equity MF) | 70% |

| Stability (Debt/Hybrid MF) | 30% |

👉 Beginners should avoid complex funds initially.

Example: Indian Middle-Class SIP Journey

Ramesh (Age 28, Private Job, Salary ₹32,000)

Starts SIP: ₹2,500/month

Annual step-up: 10%

Investment duration: 25 years

Result:

Total invested: ~₹24 lakh

Estimated value: ₹80 lakh – ₹1 crore

This is how normal people build wealth — slowly and steadily.

Best Type of SIP for Beginners

For beginners, these are safest options:

Avoid:

SIP vs RD – Which is Better for Beginners?

| Feature | SIP | RD |

|---|---|---|

| Risk | Medium | Very Low |

| Returns | 10–14% (long term) | 5–7% |

| Inflation Protection | Yes | No |

| Wealth Creation | High | Low |

👉 Best strategy: RD for emergency + SIP for growth

When Should You Increase SIP Amount?

Increase SIP when:

Salary increases

EMI reduces

Lifestyle stabilizes

Bonus or incentives received

This is called SIP Step-Up, very powerful for Indians.

Statutory Disclaimer

Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully. Past performance is not indicative of future returns. SIP returns are market-linked and not guaranteed. This article is for educational purposes only and not a recommendation. Investments should be made as per your financial goals and risk capacity, following guidelines issued by SEBI.

Frequently Asked Questions (FAQ)

Q1. Can I start SIP with ₹500?

Yes. Many mutual funds allow SIP starting from ₹500.

Q2. Is SIP safe for beginners?

SIP is safer than lump sum investment, but it still has market risk. Long-term holding reduces risk.

Q3. How long should beginners continue SIP?

Minimum 10–15 years for meaningful wealth creation.

Q4. Can I stop SIP anytime?

Yes. SIP is flexible. You can pause, stop, or modify anytime.

Q5. Is SIP better than saving account?

Yes. Savings account money loses value due to inflation. SIP helps money grow.

Useful Video & Picture Resources

SIP Explained in Hindi:

https://www.youtube.com/watch?v=8eLZK5zKkVQHow Compounding Works:

https://www.youtube.com/watch?v=H0MZ0YwG9m8SIP Growth Chart Image:

https://www.amfiindia.com/images/sip-growth.png

Suggested Internal Links for Further Study

Best Mutual Funds for SIP Beginners in India

https://marketmeterab.blogspot.com/best-mutual-funds-sip-indiaSIP vs Lumpsum – Which is Better?

https://marketmeterab.blogspot.com/sip-vs-lumpsumHow Much Money Should Indians Save Monthly?

https://marketmeterab.blogspot.com/monthly-savings-india

Final Thoughts

The best SIP amount for beginners in India is not about showing off or copying others. It is about comfort, consistency, and long-term patience.

Start small. Stay regular. Increase slowly.

That is how ordinary Indian salaries create extraordinary wealth over time.

{kind=link}

Comments

Post a Comment