Common Insurance Claim Mistakes in India: How to Avoid Rejection & Delays (2026 Guide)

Common Insurance Claim Mistakes in India: How to Avoid Rejection & Get Your Money Easily

Common Insurance Claim Mistakes in India: How to Avoid Rejection & Delays (2026 Guide)

Learn about common insurance claim mistakes in India and how to avoid rejection in health and life insurance. Simple guide with real examples and expert tips.

Indian family discussing rejected insurance claim documents

Filling insurance claim form at hospital desk India

Health insurance claim paperwork hospital billing counter

Life insurance nominee submitting claim forms India office

Rejected insurance claim due to missing documents India

In India, lakhs of people buy insurance every year.

But when the time comes to use it, many families hear one painful sentence:

❌ “Your claim has been rejected.”

❌ “Your claim is under investigation.”

❌ “Please submit more documents.”

This creates stress at the worst possible time—during illness, accident, or death.

The sad truth is:

👉 Most claim rejections happen because of small mistakes.

In this article, we will explain the most common insurance claim mistakes in India and how you can avoid them in a simple, practical, and friendly way, with real Indian examples.

No legal language. Only clear guidance.

Who Regulates Insurance Claims in India?

All insurance companies in India are regulated by:

👉 Insurance Regulatory and Development Authority of India (IRDAI)

IRDAI ensures:

✔ Fair claim process

✔ Time-bound settlement

✔ Customer protection

✔ Grievance support

So, if you follow rules properly, your claim is legally protected.

Why Insurance Claims Get Rejected in India

Before learning mistakes, understand one thing:

Insurance companies do not reject claims randomly.

They check:

✔ Policy terms

✔ Medical history

✔ Documents

✔ Payment record

✔ Truthfulness

If something is wrong, claim gets delayed or rejected.

Let us see the biggest mistakes.

1️⃣ Hiding Medical History (Biggest Mistake)

This is the No.1 reason for rejection.

Many Indians hide:

❌ Diabetes

❌ BP

❌ Heart problem

❌ Smoking habit

❌ Past surgery

They think:

“Why tell? Premium will increase.”

But later, company checks hospital records.

Then:

👉 Claim = Rejected

Example

Rohit had diabetes but did not mention it.

After 3 years, he was hospitalized.

Insurance company found old reports.

Claim rejected.

Solution

✔ Always disclose full health details

✔ Be honest in proposal form

✔ Upload correct reports

Honesty saves lakhs.

2️⃣ Not Reading Policy Terms

Most people never read policy documents.

They only see:

✔ Premium

✔ Cover amount

They ignore:

❌ Waiting period

❌ Exclusions

❌ Sub-limits

❌ Room rent cap

Later, they get shocked.

Example

Meena booked deluxe hospital room.

Policy allowed only ₹3,000/day.

Extra cost = Not paid.

Solution

✔ Read key points

✔ Ask doubts

✔ Check exclusions

✔ Save policy PDF

30 minutes reading saves ₹30,000.

3️⃣ Missing Premium Payment

Many people forget renewal.

Result:

After lapse:

❌ No protection

❌ No claim

❌ Waiting period restarts

Example

Sunil missed renewal by 2 months.

Hospitalised later.

Claim = Zero.

Solution

✔ Enable auto-debit

✔ Set phone reminder

✔ Renew before due date

Never let policy lapse.

4️⃣ Delaying Claim Intimation

Insurance companies have timelines.

You must inform them:

✔ Immediately (accident/emergency)

✔ Within 24–48 hours (hospitalisation)

If you delay:

👉 Company suspects fraud.

Example

Amit informed insurer after 10 days.

Claim went for investigation.

Payment delayed by 6 months.

Solution

✔ Call insurer immediately

✔ Use app/email

✔ Inform even from hospital

Early intimation = Faster settlement.

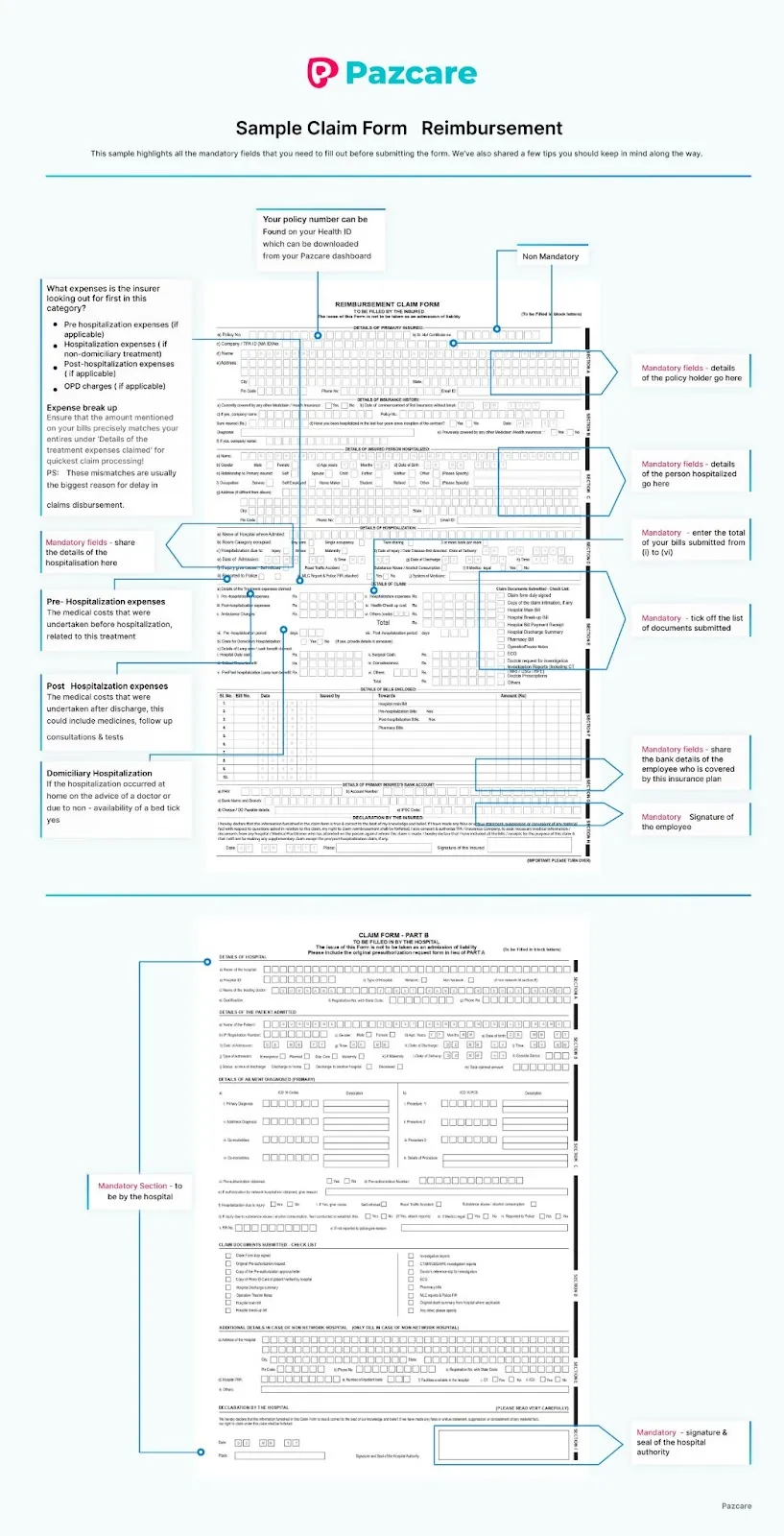

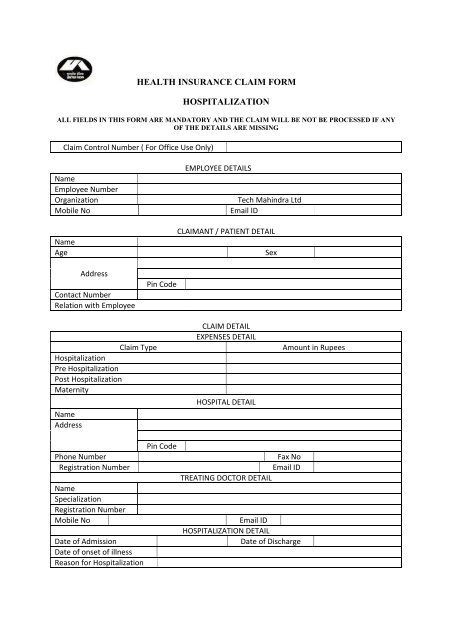

5️⃣ Incomplete Documents

Many claims fail due to missing papers.

Common missing items:

❌ Discharge summary

❌ Original bills

❌ Doctor prescription

❌ Investigation reports

❌ ID proof

Without documents, company cannot process.

Chart: Required Documents (Health Claim)

Hospital Bill

+

Discharge Summary

+

Doctor Prescription

+

Test Reports

+

ID Proof

=

Successful Claim

Solution

✔ Keep file for bills

✔ Take photos

✔ Ask hospital clearly

✔ Submit checklist-wise

Organised papers = Smooth claim.

6️⃣ Claiming for Non-Covered Treatment

Some treatments are not covered.

Example:

❌ Cosmetic surgery

❌ Weight loss surgery

❌ Fertility treatment

❌ Alternative therapy (in some plans)

People still claim.

Result:

👉 Rejection.

Solution

✔ Check coverage list

✔ Ask insurer before treatment

✔ Use customer care

Never assume “everything is covered”.

7️⃣ Using Non-Network Hospital (Without Planning)

If hospital is not in network:

✔ You must pay first

✔ Claim later (reimbursement)

Many people don’t know this.

They expect cashless.

Then struggle.

Example

Ravi went to nearby private clinic.

Not in network.

Paid ₹1.8L.

Got refund after 4 months.

Solution

✔ Check network hospitals

✔ Save list in phone

✔ Use insurer app

Prefer cashless hospitals.

8️⃣ Wrong Nominee Details (Life Insurance)

In life insurance, nominee is very important.

Common mistakes:

❌ Old nominee (not updated)

❌ No nominee

❌ Wrong relation

❌ Incomplete KYC

This causes legal delay.

Example

Suresh never updated nominee after marriage.

After death, parents and wife fought.

Claim delayed 2 years.

Solution

✔ Update nominee after marriage

✔ After child birth

✔ After divorce

Keep nominee updated.

9️⃣ Giving Wrong Information in Claim Form

Many people write:

❌ Wrong dates

❌ Wrong hospital name

❌ Wrong diagnosis

❌ Wrong expenses

Even small mistake creates doubt.

Solution

✔ Fill slowly

✔ Cross-check

✔ Ask hospital staff

✔ Keep copy

Accuracy matters.

10️⃣ Depending Only on Office Insurance

Office group insurance is risky.

Because:

❌ Ends when job ends

❌ Limited coverage

❌ Employer controls claim

When job changes, policy stops.

Example

Deepak resigned.

After 2 months, surgery needed.

No insurance.

Solution

✔ Buy personal policy

✔ Use office as extra

✔ Never depend fully

Personal policy = Permanent safety.

Real-Life Indian Case Study

Case: Mahesh (Accountant, Dhanbad)

Mistakes:

❌ Hid BP

❌ Missed renewal once

❌ Delayed intimation

Result:

Claim rejected.

Loss = ₹2.4 lakh

After learning, he bought new policy and stayed careful.

Chart: Claim Rejection Cycle

Wrong Info / Delay / Missing Docs

↓

Company Doubts

↓

Investigation

↓

Delay / Rejection

Avoid first step = Avoid problem.

Health Insurance vs Life Insurance Claim Mistakes

| Area | Health Insurance | Life Insurance |

|---|---|---|

| Main Issue | Documents | Nominee/KYC |

| Common Error | Delay | Wrong details |

| Risk | Partial payment | Long legal delay |

Both need care.

How to Ensure 100% Smooth Claim (Golden Rules)

Follow these 7 rules:

1️⃣ Disclose everything honestly

2️⃣ Read policy carefully

3️⃣ Renew on time

4️⃣ Inform early

5️⃣ Keep documents

6️⃣ Use network hospitals

7️⃣ Update nominee

Do this and your claim will be smooth.

What to Do If Your Claim Is Rejected?

Don’t panic.

Steps:

1️⃣ Ask for written reason

2️⃣ Submit clarification

3️⃣ Contact grievance cell

4️⃣ Approach IRDAI

5️⃣ Use Ombudsman (if needed)

Most genuine claims get settled later.

Tax and Claim Issues

Sometimes people make mistakes in tax-linked insurance.

Learn more:

Internal Link: Mutual Fund Taxation in India

https://marketmeterab.blogspot.com/mutual-fund-taxation-india

Insurance + Financial Planning

Claims become easier when planning is proper.

| Tool | Purpose |

|---|---|

| Health Insurance | Medical safety |

| Term Insurance | Family security |

| SIP | Wealth |

| PPF | Safety |

👉 Related Read:

Internal Link: Health Insurance Basics in India

https://marketmeterab.blogspot.com/health-insurance-basics

👉 Related Read:

Internal Link: What Is Term Insurance in India

https://marketmeterab.blogspot.com/term-insurance-india

Common Myths About Claims

❌ Myth 1: Companies Always Reject Claims

Truth: Genuine claims are mostly paid.

❌ Myth 2: Agents Will Handle Everything

Truth: You are responsible.

❌ Myth 3: Small Lies Don’t Matter

Truth: They matter most.

How to Prepare for Claims in Advance

Do this today:

✔ Keep insurance folder

✔ Share details with spouse

✔ Save helpline numbers

✔ Keep hospital list

✔ Store policy soft copy

Preparation = Peace of mind.

Statutory Disclaimer

Insurance claims are subject to terms, conditions, disclosures, and documentation requirements mentioned in the policy document. Claim approval depends on policy provisions and regulatory guidelines. This article is for educational purposes only and does not constitute legal or financial advice. Readers should carefully read policy documents and consult licensed advisors before taking decisions. All insurers are regulated by the Insurance Regulatory and Development Authority of India.

Frequently Asked Questions (FAQ)

Q1. Why are most claims rejected in India?

Mainly due to wrong information and missing documents.

Q2. Can rejected claims be reopened?

Yes, if you provide proper proof.

Q3. How long should claim settlement take?

Usually 15–30 days for complete cases.

Q4. Is hiding disease risky?

Yes. It is the biggest reason for rejection.

Q5. Should I keep medical reports?

Yes. Always keep past records.

Useful Video & Image Resources

Insurance Claim Process Explained (Hindi):

https://www.youtube.com/watch?v=F8M2Q9L7X4AHow to Avoid Claim Rejection:

https://www.youtube.com/watch?v=K9F3L2M8X7QIRDAI Official Website:

https://www.irdai.gov.inNational Health Portal:

https://www.nhp.gov.in

Bibliography

IRDAI Consumer Education Material

Insurance Act of India

Health & Life Insurance Policy Guidelines

RBI Financial Literacy Reports

Insurance Ombudsman Annual Reports

Suggested Internal Links for MarketMeterAB

Why Mediclaim Is Important in India

https://marketmeterab.blogspot.com/why-mediclaim-importantFamily Floater Health Insurance

https://marketmeterab.blogspot.com/family-floater-health-insuranceHow Much Term Insurance Do Indians Need

https://marketmeterab.blogspot.com/how-much-term-insuranceTerm Insurance vs Endowment Plan

https://marketmeterab.blogspot.com/term-vs-endowmentLong Term vs Short Term Investing

https://marketmeterab.blogspot.com/long-term-vs-short-term-investing

Final Words

Buying insurance is easy.

Getting claim is what really matters.

Most problems happen because of:

❌ Carelessness

❌ Lack of knowledge

❌ Small mistakes

If you stay alert and honest, insurance will support you when you need it most.

👉 Remember: Right information + Right documents = Guaranteed peace of mind.

Comments

Post a Comment