ELSS Mutual Funds in India Explained: Simple Tax-Saving Guide for Common Citizens

ELSS Mutual Funds in India Explained: Simple Tax-Saving Guide for Common Citizens

For most Indian citizens, one big tension comes every year between January and March:

“How do I save tax and still grow my money?”

Many people blindly invest in tax-saving FDs, insurance policies, or random schemes at the last minute. Later, they realize their money is stuck and returns are low.

This is where ELSS Mutual Funds become a smart and modern solution.

In this article, we will explain ELSS mutual funds in India in a simple, practical, and real-life manner, especially for middle-class families, salaried people, and self-employed citizens.

No complicated language. Only clear guidance.

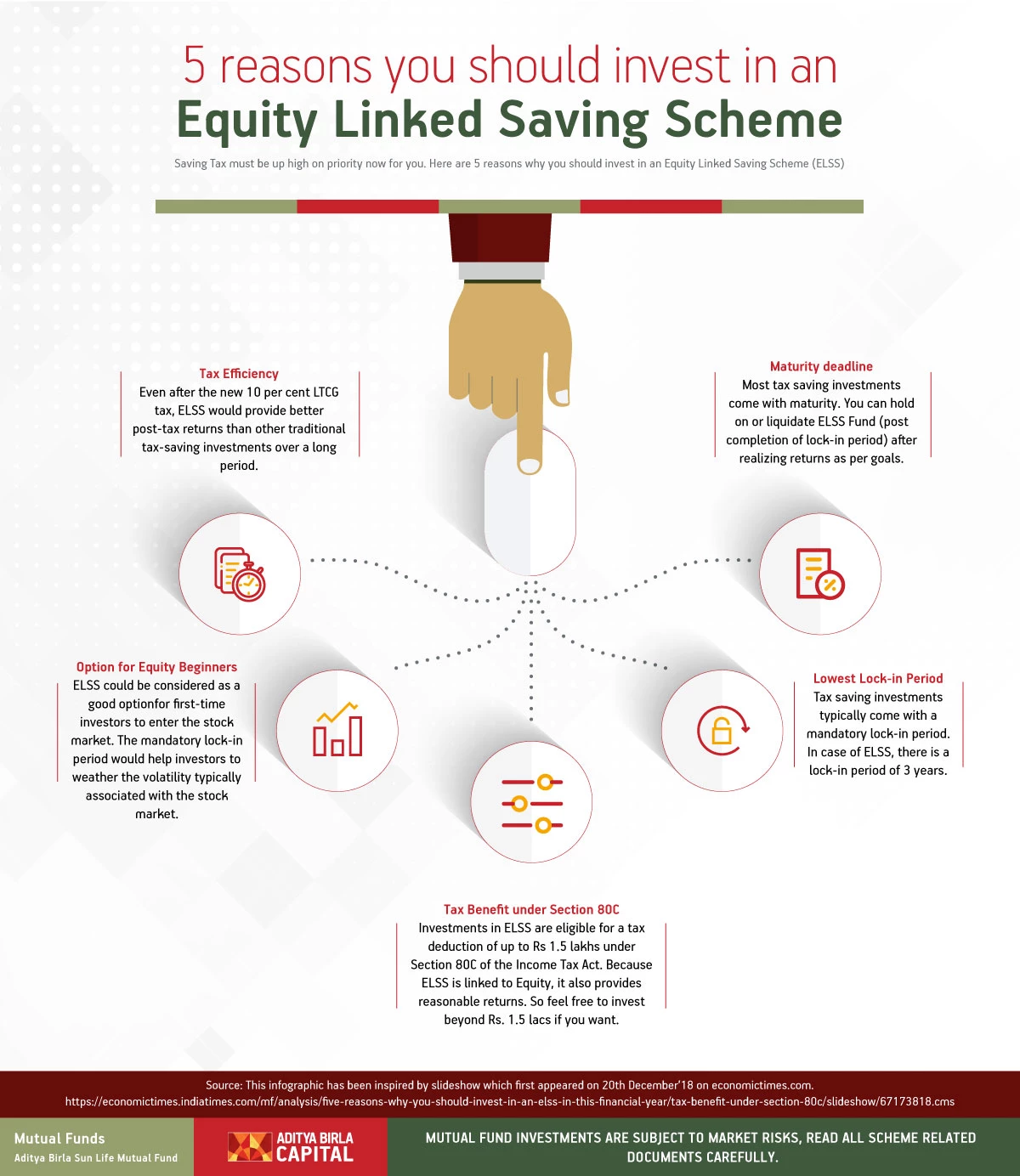

What is ELSS in Simple Words?

ELSS means Equity Linked Savings Scheme.

It is a type of mutual fund that:

Invests mainly in stock market companies

Helps you save tax under Section 80C

Has a fixed lock-in period of 3 years

Offers higher return potential than traditional options

In short:

👉 ELSS = Tax Saving + Wealth Creation

Why Was ELSS Introduced in India?

The government wanted citizens to:

Save tax

Participate in equity markets

Build long-term wealth

So, ELSS was created and regulated by SEBI to protect investors.

Today, ELSS is one of the most popular tax-saving tools for young and working Indians.

How ELSS Works: Easy Example

Let’s understand with a real-life example.

Case: Priya (IT Employee, Bengaluru)

Salary: ₹45,000/month

Annual income: ₹5.4 lakh

Tax-saving target: ₹1.5 lakh

She invests:

₹12,500/month in ELSS SIP

Total yearly investment: ₹1.5 lakh

Benefits:

✅ Saves tax

✅ Builds wealth

✅ Flexible SIP

✅ Only 3-year lock-in

After 15 years, her investment can grow to ₹40–50 lakh (approx).

That is the power of ELSS.

Tax Benefit of ELSS Under Section 80C

ELSS investments qualify under Section 80C of Income Tax Act.

Maximum Deduction

👉 Up to ₹1.5 lakh per year

This means:

| Investment | Tax Saved (30% Slab) |

|---|---|

| ₹50,000 | ₹15,000 |

| ₹1,00,000 | ₹30,000 |

| ₹1,50,000 | ₹45,000 |

So, ELSS helps you legally reduce tax burden.

ELSS Lock-In Period Explained

ELSS has a 3-year lock-in.

This is the shortest lock-in among all tax-saving options.

| Option | Lock-in |

|---|---|

| ELSS | 3 Years |

| PPF | 15 Years |

| Tax FD | 5 Years |

| NSC | 5 Years |

After 3 years, you can withdraw anytime.

This gives you freedom and flexibility.

ELSS vs Other Tax-Saving Options (Comparison Table)

| Feature | ELSS | PPF | Tax FD | NSC |

|---|---|---|---|---|

| Returns | 10–14% (Long Term) | 7–8% | 5–6% | 6–7% |

| Lock-in | 3 Years | 15 Years | 5 Years | 5 Years |

| Risk | Medium-High | Very Low | Very Low | Low |

| Tax Benefit | Yes | Yes | Yes | Yes |

| Wealth Creation | High | Medium | Low | Low |

👉 ELSS is best for long-term wealth builders.

SIP vs Lump Sum in ELSS

You can invest in ELSS in two ways:

1. SIP in ELSS (Recommended)

Monthly investment

Less market risk

Better discipline

Example:

₹3,000/month × 12 = ₹36,000/year

2. Lump Sum in ELSS

One-time investment

More risk

Needs timing

Best for bonus/inheritance money.

👉 Related Read:

Internal Link: SIP vs Lump Sum in India

https://marketmeterab.blogspot.com/sip-vs-lumpsum

Returns from ELSS: What Can You Expect?

Historically, good ELSS funds have delivered:

10% to 14% CAGR (long term)

Some years negative

Some years very high

Example (15 Years Investment)

| Monthly SIP | Total Invested | Approx Value |

|---|---|---|

| ₹2,000 | ₹3.6 lakh | ₹9–11 lakh |

| ₹5,000 | ₹9 lakh | ₹25–30 lakh |

| ₹10,000 | ₹18 lakh | ₹50+ lakh |

⚠️ Returns are not guaranteed. Market risk exists.

Who Should Invest in ELSS?

ELSS is suitable for:

✅ Salaried employees

✅ Self-employed professionals

✅ Small business owners

✅ First-time investors

✅ Young earners

Not ideal for:

❌ Senior citizens needing fixed income

❌ People afraid of market ups and downs

How to Choose a Good ELSS Fund?

Check these 5 points:

1. Fund History

Minimum 5–7 years track record

2. Fund Manager

Experienced manager is better

3. Expense Ratio

Lower is better

4. Consistency

Stable returns over years

5. AMC Reputation

Trusted fund houses

👉 Related Guide:

Internal Link: Best Mutual Funds for Beginners

https://marketmeterab.blogspot.com/best-mutual-funds-india

ELSS and Capital Gains Tax

ELSS is an equity fund. So:

Long-term capital gains above ₹1.25 lakh/year are taxable

Tax rate: 10% (as per current rules)

Gains below limit: Tax-free

Each SIP installment is treated separately for lock-in and tax.

Common Mistakes Indians Make in ELSS

Investing only in March (last minute)

Choosing fund based on ads

Stopping SIP in market fall

Not reviewing portfolio

Expecting quick profit

Avoid these mistakes for better results.

Best ELSS Strategy for Indians

Ideal Formula

👉 ELSS + SIP + Long Term + Review

Example Plan:

Start at age 25

₹3,000/month ELSS SIP

Increase 10% yearly

Continue till 45

Result: Strong retirement + tax savings

Statutory Disclaimer

Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully. Past performance is not indicative of future returns. This article is for educational purposes only and does not constitute investment advice. Investors should take decisions based on their financial goals and risk profile in accordance with guidelines issued by SEBI.

Frequently Asked Questions (FAQ)

Q1. Is ELSS safe for beginners?

Yes, if you invest through SIP and stay long term.

Q2. Can I withdraw ELSS after 3 years?

Yes, after lock-in you can redeem anytime.

Q3. Can I invest more than ₹1.5 lakh?

Yes, but tax benefit is limited to ₹1.5 lakh.

Q4. Is ELSS better than PPF?

For long-term wealth, yes. For safety, PPF is better.

Q5. Can I have multiple ELSS funds?

Yes, but 2–3 good funds are enough.

Useful Video & Image Resources

ELSS Explained in Hindi:

https://www.youtube.com/watch?v=Q5Gk3JtKp9ETax Saving Mutual Funds Guide:

https://www.youtube.com/watch?v=9K8R7D2sXWcELSS Comparison Chart:

https://www.amfiindia.com/images/elss-comparison.png

Bibliography

AMFI India Mutual Fund Reports

Income Tax Act – Section 80C

NSE Market Performance Data

Mutual Fund Scheme Documents

Suggested Internal Links for MarketMeterAB

Best SIP Amount for Beginners

https://marketmeterab.blogspot.com/best-sip-amount-indiaLarge Cap vs Mid Cap vs Small Cap

https://marketmeterab.blogspot.com/large-mid-small-capHow to Build Wealth in India

https://marketmeterab.blogspot.com/wealth-building-india

Final Words

ELSS is not just a tax-saving tool.

It is a wealth-building habit.

If you start early, invest regularly, and stay patient, ELSS can help you:

✅ Save tax every year

✅ Beat inflation

✅ Build financial confidence

👉 Smart Indians don’t run from tax. They plan for it. And ELSS is one of their best tools.

{kind=link}

Comments

Post a Comment