EPF vs PPF Difference in India Explained: Which Is Better for You? (Beginner Guide 2026)

EPF vs PPF Difference in India Explained: Simple Guide for Safe Retirement Planning

EPF vs PPF Difference in India Explained: Which Is Better for You? (Beginner Guide 2026)

Understand the difference between EPF and PPF in India with simple examples, returns, tax benefits, rules, and calculations. Easy guide for salaried and self-employed citizens.

EPF passbook UAN portal balance check India example

PPF passbook post office bank savings account India

EPF vs PPF comparison chart infographic India

Indian employee checking EPF balance mobile app screen

PPF account opening form India post office bank process

For most Indian citizens, especially salaried employees and middle-class families, one big question comes again and again:

“Should I rely on EPF or PPF for my future?”

“Which one gives better returns and safety?”

Many people invest in both, but very few clearly understand the difference.

So in this article, we will explain EPF vs PPF in India in a simple, practical, and friendly way, using real Indian examples.

No complicated finance terms. Only clear and useful guidance.

What Is EPF? (In Simple Words)

EPF (Employees’ Provident Fund) is a retirement savings scheme for salaried employees.

It is managed by:

👉 Employees' Provident Fund Organisation (EPFO)

If you work in a private company with more than 20 employees, EPF is usually mandatory.

How EPF Works

Every month:

Employee contributes 12% of basic salary

Employer also contributes 12%

Money goes to EPF account

So, savings happen automatically.

Example (EPF)

Rohit earns ₹25,000 basic salary.

His EPF = ₹3,000/month

Employer EPF = ₹3,000/month

Total = ₹6,000/month

Yearly = ₹72,000

Without effort, he saves for retirement.

What Is PPF? (In Simple Words)

PPF (Public Provident Fund) is a voluntary long-term savings scheme.

It is backed by the Government of India and regulated by:

👉 Ministry of Finance (India)

Anyone can open PPF:

✅ Salaried

✅ Self-employed

✅ Business owners

✅ Housewives

✅ Students

You decide how much to invest.

How PPF Works

You invest between ₹500 and ₹1.5 lakh per year

Lock-in: 15 years

Interest: Decided by government

It is fully voluntary.

Example (PPF)

Meena invests ₹1,00,000 every year in PPF.

After 15 years, she builds a big tax-free fund.

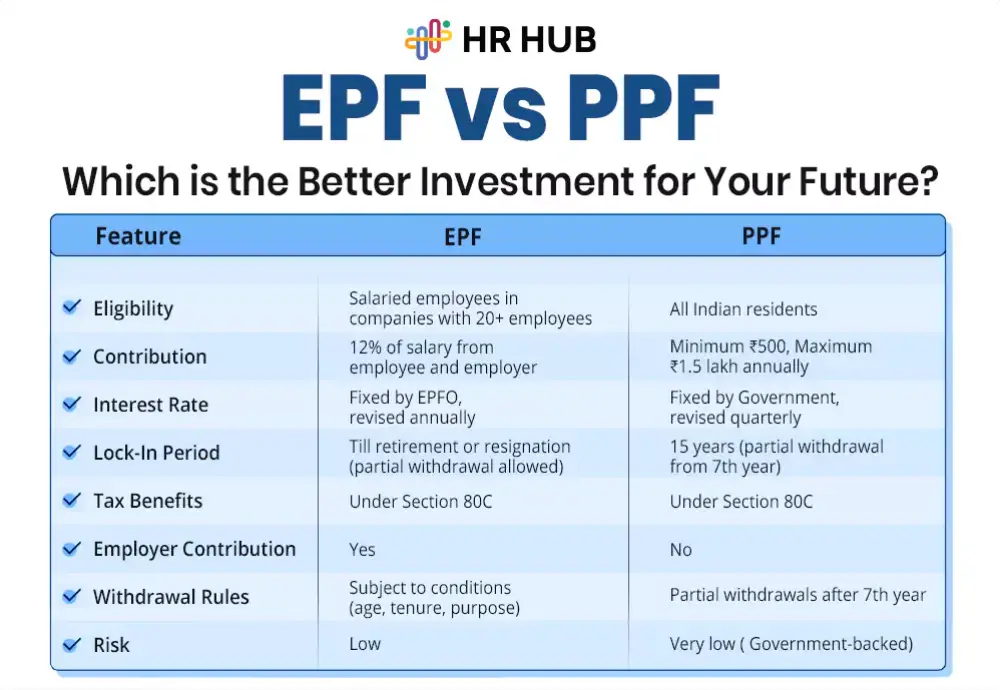

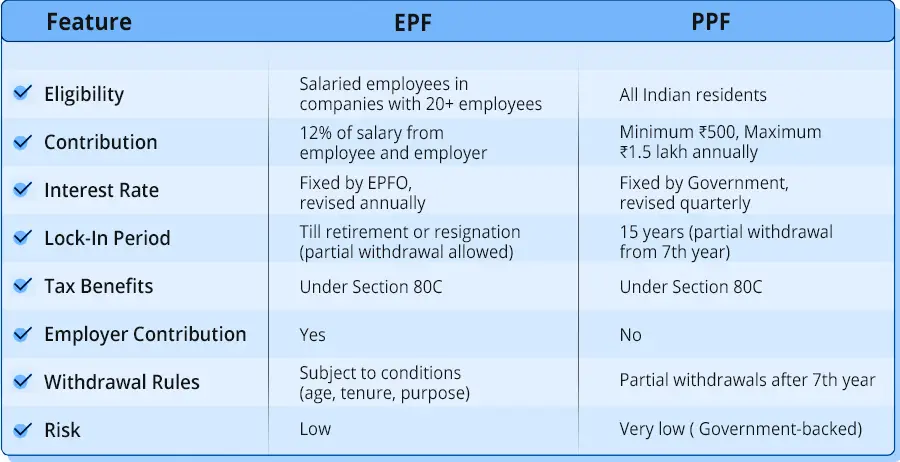

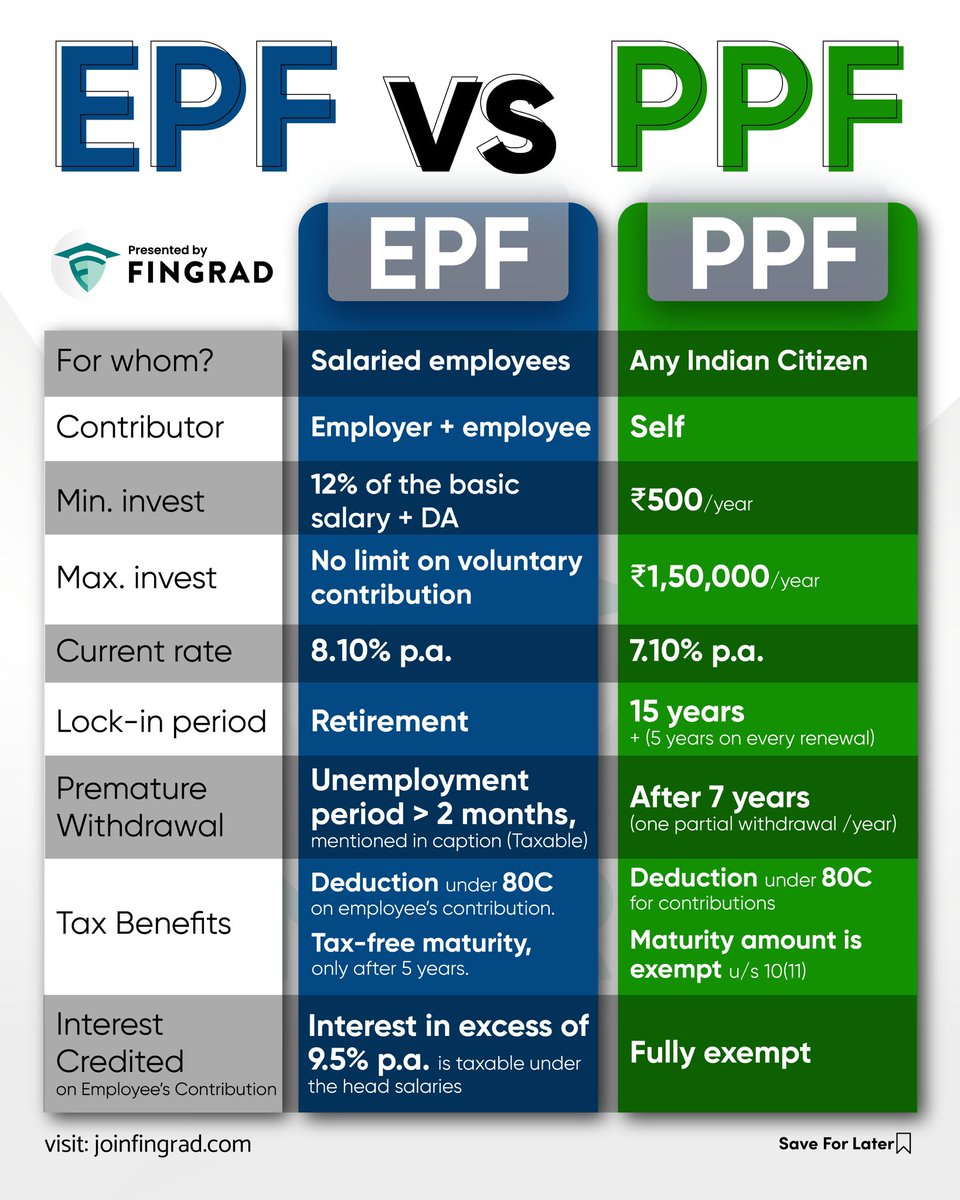

EPF vs PPF: Basic Difference Table

| Feature | EPF | PPF |

|---|---|---|

| Who Can Invest | Salaried Employees | All Citizens |

| Contribution | Mandatory | Voluntary |

| Lock-in | Till Job Change/Retirement | 15 Years |

| Max Limit | No Fixed Limit | ₹1.5 Lakh/Year |

| Risk | Very Low | Very Low |

| Control | Employer + EPFO | You |

👉 EPF = Job-linked

👉 PPF = Self-controlled

Interest Rate: EPF vs PPF

Interest rates change every year.

| Scheme | Avg Interest (Approx) |

|---|---|

| EPF | 8% – 8.5% |

| PPF | 7% – 8% |

Both are better than normal savings accounts.

Tax Benefit: EPF vs PPF (EEE Advantage)

Both EPF and PPF follow EEE system:

| Stage | EPF | PPF |

|---|---|---|

| Investment | Tax-Free (80C) | Tax-Free (80C) |

| Interest | Tax-Free | Tax-Free |

| Maturity | Tax-Free* | Tax-Free |

(*Conditions apply for EPF withdrawal.)

This makes both very powerful.

👉 Related Read:

Internal Link: Mutual Fund Taxation in India

https://marketmeterab.blogspot.com/mutual-fund-taxation-india

Withdrawal Rules: EPF vs PPF

EPF Withdrawal

You can withdraw:

✅ After retirement

✅ After job loss (2 months)

✅ For house, marriage, medical, etc.

Partial withdrawals allowed.

PPF Withdrawal

Partial withdrawal after 7 years

Full after 15 years

Extension possible

PPF is stricter.

Chart: Withdrawal Timeline

EPF → Job Change / Emergency / Retirement

PPF → 7 Years (Partial) → 15 Years (Full)

EPF is more flexible.

Calculation Example: EPF vs PPF (15 Years)

Let us compare with real numbers.

Case 1: EPF Investment

Amit’s EPF saving = ₹6,000/month

Yearly = ₹72,000

Interest = 8.25%

Period = 15 Years

👉 Total Invested ≈ ₹10.8 lakh

👉 Maturity Value ≈ ₹25–28 lakh

Case 2: PPF Investment

Rina invests ₹72,000/year in PPF

Interest = 7.5%

Period = 15 Years

👉 Total Invested ≈ ₹10.8 lakh

👉 Maturity Value ≈ ₹19–21 lakh

Result

EPF gives higher return because of employer contribution.

EPF vs PPF: Risk and Safety

| Factor | EPF | PPF |

|---|---|---|

| Government Support | Yes | Yes |

| Market Risk | No | No |

| Default Risk | Very Low | Very Low |

| Stability | High | Very High |

Both are among the safest investments in India.

Who Should Choose EPF?

EPF is best for:

✅ Private sector employees

✅ People who want automatic savings

✅ Those with long-term jobs

✅ Beginners in investing

If you have EPF, never ignore it.

It is free money from employer.

Who Should Choose PPF?

PPF is best for:

✅ Self-employed people

✅ Freelancers

✅ Small business owners

✅ Housewives

✅ Conservative investors

PPF gives full control.

Can You Use Both EPF and PPF? (Best Strategy)

Yes. Smart Indians use both.

Ideal Combination

| Source | Allocation |

|---|---|

| EPF | Mandatory Base |

| PPF | Voluntary Top-Up |

| SIP/Equity | Growth |

This creates:

👉 Safety + Growth + Tax Saving

👉 Related Read:

Internal Link: Long Term vs Short Term Investing

https://marketmeterab.blogspot.com/long-term-vs-short-term-investing

Real-Life Indian Example

Case: Prakash (Sales Executive, Surat)

EPF: ₹5,000/month

PPF: ₹50,000/year

SIP: ₹2,000/month

After 20 years:

EPF Corpus: ₹35+ lakh

PPF Corpus: ₹18+ lakh

SIP Corpus: ₹25+ lakh

Total ≈ ₹78 lakh+

Balanced planning works.

EPF vs PPF vs Mutual Funds

| Feature | EPF | PPF | Mutual Fund |

|---|---|---|---|

| Risk | Very Low | Very Low | Medium |

| Return | Medium | Medium | High (Long Term) |

| Lock-in | Job Based | 15 Years | Flexible |

| Suitable | Salaried | All | Growth Seekers |

👉 For best results: Use all three.

👉 Related Read:

Internal Link: Best SIP Amount for Beginners

https://marketmeterab.blogspot.com/best-sip-amount-india

Common Mistakes Indians Make

Ignoring EPF statements

Not checking UAN balance

Missing PPF yearly deposit

Withdrawing early

Depending only on EPF/PPF

Avoid these mistakes.

How to Check EPF and PPF Balance

EPF

EPFO App

SMS service

PPF

Bank Net Banking

Passbook

Post Office portal

Check once every 3 months.

Role of Market Regulator

While EPF and PPF are government schemes, market investments are regulated by:

👉 Securities and Exchange Board of India (SEBI)

So, your overall financial system is well protected.

Statutory Disclaimer

EPF and PPF rules, interest rates, and tax benefits are subject to change as per Government of India notifications. This article is for educational purposes only and does not constitute financial advice. Investors should assess their financial goals and consult a qualified advisor before making decisions. Market-linked investments are regulated by Securities and Exchange Board of India.

Frequently Asked Questions (FAQ)

Q1. Is EPF better than PPF?

For salaried people, yes. Because of employer contribution.

Q2. Can I invest in both?

Yes. It is recommended.

Q3. Is PPF safer than EPF?

Both are equally safe.

Q4. Can I withdraw EPF anytime?

Only under specific conditions.

Q5. Which is best for retirement?

EPF + PPF + SIP together.

Useful Video & Image Resources

EPF vs PPF Explained (Hindi):

https://www.youtube.com/watch?v=F8Q2M9L7X4AHow EPF Works:

https://www.youtube.com/watch?v=K7M2F9QX4P8EPFO Portal:

https://www.epfindia.gov.in

Bibliography

EPFO Annual Reports

Ministry of Finance Notifications

RBI Financial Stability Reports

Government Savings Scheme Guidelines

Suggested Internal Links for MarketMeterAB

PPF in India Explained with Calculation

https://marketmeterab.blogspot.com/ppf-india-explainedWhat Is Stock Market in India

https://marketmeterab.blogspot.com/what-is-stock-market-indiaHow to Open Demat Account in India

https://marketmeterab.blogspot.com/how-to-open-demat-accountELSS Mutual Funds Explained

https://marketmeterab.blogspot.com/elss-mutual-funds-indiaCharges in Stock Trading Explained

https://marketmeterab.blogspot.com/stock-trading-charges-india

Final Words

EPF and PPF are like two strong pillars of Indian financial life.

EPF gives automatic savings.

PPF gives personal control.

If you use both wisely and add some growth investment, you can build:

👉 A safe, stable, and stress-free future.

Remember: Strong foundation first. High growth later.

Comments

Post a Comment