Mutual Fund Taxation in India Explained: Simple Guide for Common Citizens

Mutual Fund Taxation in India Explained: Simple Guide for Common Citizens

For many Indian citizens, investing in mutual funds has become a regular habit. SIPs, ELSS, index funds, and hybrid funds are now part of middle-class financial life.

But one topic still confuses most people:

“How much tax do I have to pay on mutual fund returns?”

Many investors focus only on returns and forget taxation. Later, when tax notices or deductions happen, they feel shocked.

This article explains mutual fund taxation in India in a simple, practical, and realistic way, using everyday Indian examples — no complicated legal language.

Why You Must Understand Mutual Fund Taxation

Knowing tax rules helps you:

✅ Avoid penalties

✅ Plan investments better

✅ Maximize net returns

✅ Reduce stress during filing

✅ Use legal tax benefits

Smart investors don’t just earn returns.

They protect those returns from unnecessary tax.

Who Controls Mutual Fund Rules in India?

Mutual funds and their taxation are regulated by:

Income Tax Department (India)

These bodies ensure investor protection and proper tax collection.

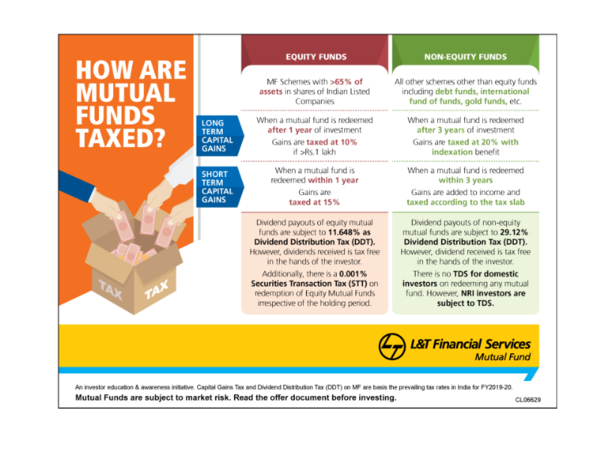

Two Main Types of Mutual Funds (For Tax Purpose)

For taxation, mutual funds are mainly divided into:

| Type | Investment Style |

|---|---|

| Equity Funds | Invest mostly in shares |

| Debt Funds | Invest in bonds, FD-like instruments |

Hybrid funds are taxed based on equity or debt exposure.

Understanding this is very important.

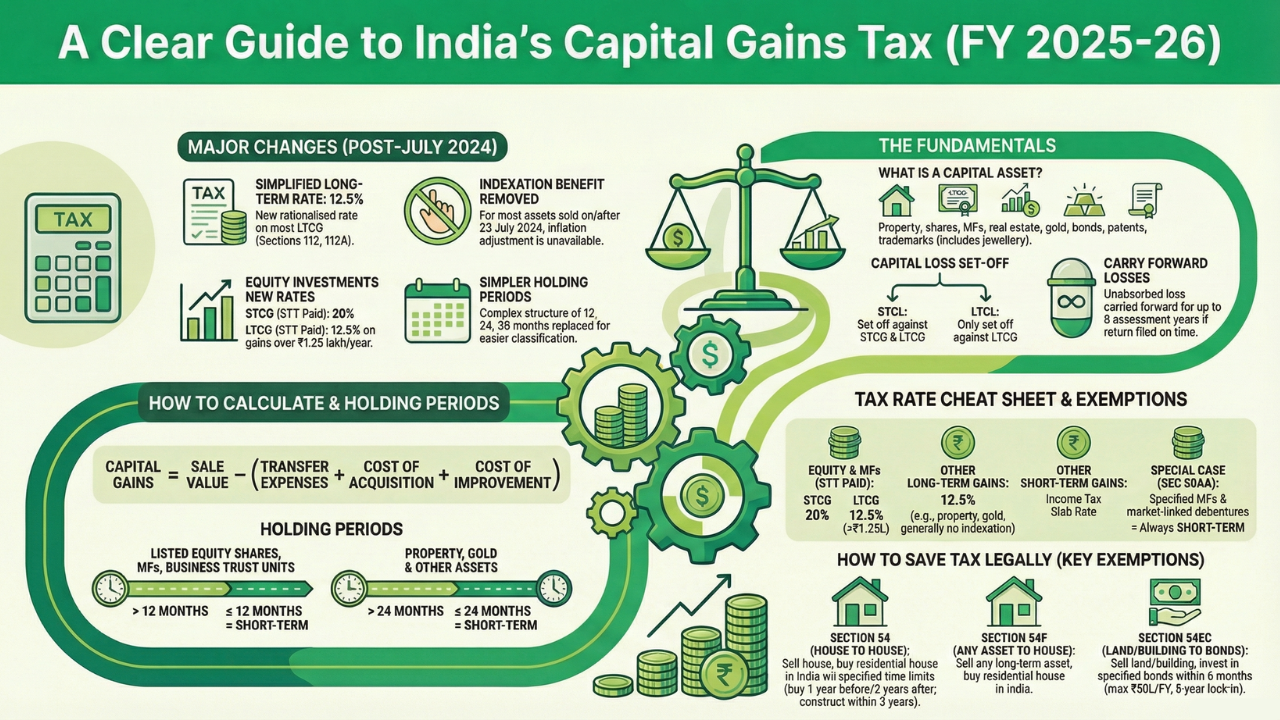

Taxation of Equity Mutual Funds in India

Equity mutual funds invest more than 65% in stocks.

They enjoy better tax treatment.

Equity Fund Capital Gains Rules

1. Short-Term Capital Gains (STCG)

If you sell before 1 year:

👉 Tax = 20%

2. Long-Term Capital Gains (LTCG)

If you sell after 1 year:

👉 Gains up to ₹1.25 lakh/year = Tax-Free

👉 Above ₹1.25 lakh = 10% tax

Equity Fund Example (Simple)

Case: Rohit (Delhi, IT Professional)

Invested: ₹2,00,000

Sold after 2 years

Value: ₹3,80,000

Profit: ₹1,80,000

Tax Calculation:

Exempt: ₹1,25,000

Taxable: ₹55,000

Tax (10%): ₹5,500

👉 Rohit keeps most of his profit.

That’s why equity funds are popular.

Taxation of Debt Mutual Funds in India

Debt funds invest in:

Government bonds

Corporate bonds

Treasury bills

Money market instruments

They are safer but taxed differently.

Debt Fund Capital Gains Rules (New System)

From recent tax changes:

👉 All debt funds are taxed as per income slab, regardless of holding period.

This means:

| Your Tax Slab | Tax on Debt Fund |

|---|---|

| 5% | 5% |

| 20% | 20% |

| 30% | 30% |

Indexation benefit is mostly removed.

Debt Fund Example

Case: Meena (Jaipur, Small Business Owner)

Invested: ₹3,00,000

Profit: ₹60,000

Tax slab: 20%

Tax = 20% of ₹60,000 = ₹12,000

Net gain = ₹48,000

👉 Not as tax-friendly as earlier.

Taxation of ELSS Mutual Funds

ELSS is special because it offers tax saving.

Benefits:

✅ Deduction under Section 80C (up to ₹1.5 lakh)

✅ 3-year lock-in

✅ Equity taxation after lock-in

After 3 years, ELSS is treated like equity fund.

👉 Related Read:

Internal Link: ELSS Mutual Funds Explained

https://marketmeterab.blogspot.com/elss-mutual-funds-india

SIP Taxation: How Is SIP Taxed?

Many people think SIP has separate tax rules.

It doesn’t.

Each SIP installment is treated as new investment.

SIP Example

You invest ₹5,000/month for 2 years.

You made 24 SIPs.

Each SIP has:

Separate purchase date

Separate tax calculation

Separate holding period

So, while redeeming, some units may be LTCG, some STCG.

👉 Related Guide:

Internal Link: Best SIP Amount for Beginners

https://marketmeterab.blogspot.com/best-sip-amount-india

Dividend Taxation in Mutual Funds

Earlier, dividends were tax-free.

Now, they are taxed.

Current Rule:

👉 Dividend = Added to your income

👉 Tax = As per slab rate

Also, 10% TDS may be deducted if dividend > ₹5,000/year.

So, growth option is usually better.

Mutual Fund Tax Comparison Chart

| Fund Type | STCG | LTCG | Best For |

|---|---|---|---|

| Equity | 20% | 10% (Above ₹1.25L) | Long term wealth |

| Debt | Slab Rate | Slab Rate | Short-term parking |

| ELSS | 20% | 10% | Tax saving |

| Hybrid (Equity) | 20% | 10% | Balanced investors |

How to Save Tax on Mutual Funds (Legal Ways)

1. Use LTCG Limit Fully

Plan withdrawals so that yearly gains stay near ₹1.25 lakh.

2. Prefer Growth Option

Avoid dividend plans unless you need regular income.

3. Invest Through ELSS

Get double benefit: tax saving + growth.

4. Hold for Long Term

Longer holding = lower tax.

5. Use Capital Loss Adjustment

Losses can be set off against gains.

Capital Loss Set-Off Rules

| Loss Type | Can Set Off Against |

|---|---|

| STCL | STCG + LTCG |

| LTCL | Only LTCG |

Unused loss can be carried forward for 8 years.

Very useful for active investors.

Real-Life Tax Planning Example

Case: Sanjay (Mumbai, Salary ₹50,000)

Investments:

ELSS: ₹1.5 lakh

Equity MF: ₹3 lakh

SIP: ₹4,000/month

After 10 years:

Total profit: ₹6 lakh

Withdraws yearly: ₹1.2 lakh

Result:

No LTCG tax (within limit)

Section 80C benefit

Smart planning

👉 Sanjay saves ₹50,000+ tax over years.

Mutual Fund Taxation vs FD Taxation

| Feature | Mutual Fund | Fixed Deposit |

|---|---|---|

| Returns | Higher | Lower |

| Tax | On gains | On interest |

| Flexibility | High | Low |

| Inflation Protection | Yes | No |

👉 Mutual funds are more tax-efficient long term.

Common Tax Mistakes Indians Make

Ignoring LTCG limit

Not keeping statements

Panic selling

Choosing dividend blindly

Not filing capital gains properly

Avoid these to stay tension-free.

Statutory Disclaimer

Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully. Past performance is not indicative of future returns. This article is for educational purposes only and does not constitute tax or investment advice. Tax laws may change. Investors should consult a qualified tax advisor and follow guidelines issued by Securities and Exchange Board of India and the Income Tax Department before investing.

Frequently Asked Questions (FAQ)

Q1. Is mutual fund profit taxable?

Yes, depending on fund type and holding period.

Q2. Is SIP tax-free?

No. SIP is taxed like normal mutual fund.

Q3. Do I pay tax every year?

Only when you redeem or receive dividends.

Q4. Is ELSS completely tax-free?

No. Only deduction is tax-free. Gains are taxed later.

Q5. Should senior citizens invest in mutual funds?

Yes, but with safer funds and proper planning.

Useful Video & Image Resources

Mutual Fund Tax Explained (Hindi):

https://www.youtube.com/watch?v=R7QK9L2F4xACapital Gains Tax India:

https://www.youtube.com/watch?v=K9F2M7T8XQ0Taxation Chart (AMFI):

https://www.amfiindia.com/images/mf-taxation.png

Bibliography

SEBI Investor Education Portal

Income Tax Act – Capital Gains Provisions

AMFI Mutual Fund Handbook

NSE & BSE Market Reports

Mutual Fund Scheme Documents

Suggested Internal Links for MarketMeterAB

SIP vs Lump Sum Investment in India

https://marketmeterab.blogspot.com/sip-vs-lumpsumELSS Mutual Funds Explained

https://marketmeterab.blogspot.com/elss-mutual-funds-indiaLarge Cap vs Mid Cap vs Small Cap

https://marketmeterab.blogspot.com/large-mid-small-capHow to Build Wealth in India

https://marketmeterab.blogspot.com/wealth-building-india

Final Thoughts

Mutual fund taxation is not difficult.

It becomes difficult only when you ignore it.

If you:

✅ Understand fund types

✅ Hold long term

✅ Use tax limits wisely

✅ Plan withdrawals

Then you can enjoy maximum returns with minimum tax.

👉 Remember: Earning money is good. Keeping it is smarter.

{kind=link}

Comments

Post a Comment