NPS Scheme in India Explained: Benefits, Tax Saving & Retirement Calculation (2026 Guide)

NPS Scheme in India Explained: Simple Guide for Retirement Planning

NPS Scheme in India Explained: Benefits, Tax Saving & Retirement Calculation (2026 Guide)

Learn how NPS works in India with simple examples, tax benefits under 80CCD, asset allocation, withdrawal rules, and retirement calculation. Beginner-friendly guide.

NPS PRAN card India retirement account example

NPS asset allocation equity debt government bonds chart India

NPS tax benefit 80CCD calculation infographic India

Indian retirement planning with NPS scheme visual guide

NPS online registration process India screenshot example

For most Indian citizens, retirement feels far away. Many people think:

“I will plan later.”

“EPF is enough.”

“Government will take care.”

But the truth is simple:

👉 Retirement planning must start early.

One powerful tool available in India is:

👉 NPS – National Pension System

In this article, we will explain NPS scheme in India in a simple, practical, and friendly way, using real Indian examples.

No complicated pension formulas. Only clear guidance.

What Is NPS? (In Simple Words)

NPS (National Pension System) is a government-backed retirement savings scheme.

It helps you:

✅ Invest regularly

✅ Save tax

✅ Build retirement corpus

✅ Get pension after 60

It was launched by the Government of India and regulated by:

👉 Pension Fund Regulatory and Development Authority (PFRDA)

Who Can Open NPS?

Anyone between 18 to 70 years can open NPS:

Salaried employees

Self-employed

Business owners

Professionals

NRIs

It is open to all Indian citizens.

How NPS Works (Step-by-Step)

Let’s understand in simple steps.

Step 1: Open NPS Account

You get a PRAN (Permanent Retirement Account Number).

This is your unique pension ID.

Step 2: Invest Regularly

You contribute money:

Monthly

Quarterly

Yearly

Minimum contribution required to keep account active.

Step 3: Money Gets Invested

Your money is invested in:

Equity (shares)

Government bonds

Corporate bonds

You choose asset allocation.

Step 4: Retirement at 60

At age 60:

You can withdraw 60% lump sum

40% must be used to buy annuity (pension)

This ensures regular income after retirement.

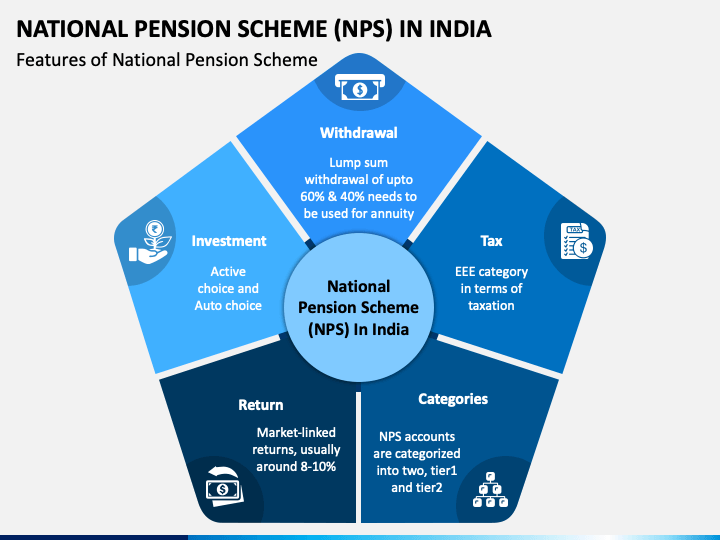

Types of NPS Accounts

There are two main types.

1️⃣ Tier 1 Account (Main Retirement Account)

Mandatory for pension

Lock-in till 60

Tax benefits available

Best for retirement planning.

2️⃣ Tier 2 Account (Voluntary Savings)

No lock-in

No special tax benefit (except govt employees)

Flexible withdrawal

Acts like mutual fund.

NPS Asset Allocation Options

You can choose how your money is invested.

Auto Choice

Allocation changes automatically with age.

More equity when young.

More debt when older.

Active Choice

You decide:

| Asset Class | Meaning |

|---|---|

| E | Equity |

| C | Corporate Bonds |

| G | Government Bonds |

Maximum equity allowed: 75% (for young investors).

Example: NPS Investment Calculation

Let us understand with real numbers.

Case: Rahul (Age 30, IT Employee)

Invests ₹5,000 per month

Annual = ₹60,000

Duration = 30 years

Average return = 10%

Total Invested:

₹18 lakh

Approx Retirement Corpus:

₹1 crore+

At 60:

60% withdrawal = ₹60 lakh

40% annuity = ₹40 lakh

Monthly pension starts.

Chart: NPS Growth Example (₹5,000 Monthly)

Age 30 → Start

Age 40 → ₹12–15 lakh

Age 50 → ₹40–50 lakh

Age 60 → ₹1 crore+

Compounding works strongly in long duration.

NPS Tax Benefits (Very Important)

NPS gives extra tax benefit.

Under:

👉 Section 80CCD(1)

Up to ₹1.5 lakh (included in 80C limit)

👉 Section 80CCD(1B)

Extra ₹50,000 deduction

So total tax benefit:

👉 ₹2 lakh possible

Example

If you invest ₹2 lakh in NPS:

Tax saving (30% slab) = ₹60,000

Big benefit.

👉 Related Read:

Internal Link: PPF in India Explained

https://marketmeterab.blogspot.com/ppf-india-explained

NPS vs EPF vs PPF

| Feature | NPS | EPF | PPF |

|---|---|---|---|

| Risk | Medium | Low | Very Low |

| Return | 8–12% | 8–8.5% | 7–8% |

| Lock-in | Till 60 | Job-based | 15 Years |

| Tax Benefit | High | Yes | Yes |

| Pension | Yes | No | No |

NPS gives highest growth potential among three.

NPS Withdrawal Rules

Before 60:

Partial withdrawal allowed (conditions apply)

After 60:

60% tax-free withdrawal

40% annuity mandatory

After 75:

Full withdrawal allowed.

Real-Life Indian Example

Case: Neha (Self-employed, Pune)

No EPF

Invests ₹8,000/month in NPS

Also invests ₹5,000 SIP

After 30 years:

NPS corpus = ₹1.6 crore

SIP corpus = ₹1.2 crore

Total retirement corpus = ₹2.8 crore

Balanced planning works.

Who Should Invest in NPS?

Best for:

✅ Salaried employees

✅ Self-employed

✅ Taxpayers in 20–30% slab

✅ Long-term planners

✅ Retirement-focused people

Not ideal for:

❌ Short-term investors

❌ People needing liquidity

NPS vs Mutual Funds

| Feature | NPS | Mutual Funds |

|---|---|---|

| Lock-in | Till 60 | Flexible |

| Tax Benefit | Extra ₹50K | No extra |

| Equity Limit | 75% | No limit |

| Pension | Yes | No |

Best strategy:

👉 NPS + Mutual Funds

👉 Related Read:

Internal Link: Long Term vs Short Term Investing

https://marketmeterab.blogspot.com/long-term-vs-short-term-investing

Common Mistakes Indians Make

Starting late

Not claiming extra ₹50K deduction

Ignoring asset allocation

Withdrawing early

Depending only on EPF

Avoid these mistakes.

How to Open NPS Account

You can open NPS:

Online through NSDL portal

Through banks

Through Post Office

Documents required:

PAN

Aadhaar

Bank account

Photo

Process is simple and online.

Role of Market Regulator

While NPS is regulated by PFRDA, stock investments in NPS are linked to markets regulated by:

👉 Securities and Exchange Board of India

So overall system is transparent.

Statutory Disclaimer

Investments in NPS are subject to market risks as returns depend on asset allocation and market performance. Past performance does not guarantee future results. Tax benefits are subject to change as per Government of India regulations. This article is for educational purposes only and does not constitute financial advice. Investors should consult a qualified advisor before making decisions.

Frequently Asked Questions (FAQ)

Q1. Is NPS safe?

Yes, but returns depend on market performance.

Q2. Can I withdraw full amount at 60?

Only 60% lump sum. 40% must buy annuity.

Q3. Is NPS better than PPF?

For higher growth, yes. For safety, PPF is better.

Q4. Can self-employed invest?

Yes, highly recommended.

Q5. What happens if I stop contribution?

Account may become inactive but can be reactivated.

Useful Video & Image Resources

NPS Explained in Hindi:

https://www.youtube.com/watch?v=F9L2Q8M7X4ANPS Tax Benefit Explained:

https://www.youtube.com/watch?v=K8F2M9L4X7PNPS Official Portal:

https://www.npscra.nsdl.co.inPFRDA Official Website:

https://www.pfrda.org.in

Bibliography

PFRDA Annual Reports

Ministry of Finance Notifications

Income Tax Act – Section 80CCD

RBI Financial Stability Reports

NPS Scheme Documents

Suggested Internal Links for MarketMeterAB

EPF vs PPF Difference Explained

https://marketmeterab.blogspot.com/epf-vs-ppf-differencePPF in India Explained

https://marketmeterab.blogspot.com/ppf-india-explainedSIP vs Lump Sum Investment

https://marketmeterab.blogspot.com/sip-vs-lumpsumHow Dividends Work in India

https://marketmeterab.blogspot.com/how-dividends-workWhat Is Stock Market in India

https://marketmeterab.blogspot.com/what-is-stock-market-india

Final Words

NPS is not for quick money.

It is for:

✅ Discipline

✅ Long-term planning

✅ Tax saving

✅ Secure retirement

If you start early and stay consistent, NPS can build a powerful retirement fund.

👉 Remember: Retirement planning is not about age 60. It is about starting at 30.

Comments

Post a Comment