PPF in India Explained with Calculation: Interest, Returns & 15-Year Growth Example (2026 Guide)

PPF in India Explained with Calculation: Simple Guide for Safe Long-Term Savings

PPF in India Explained with Calculation: Interest, Returns & 15-Year Growth Example (2026 Guide).

Learn how PPF works in India with simple calculations, interest rate, tax benefits, maturity rules, and real examples. Beginner-friendly guide for safe long-term savings.

Public Provident Fund PPF India passbook savings example

PPF interest calculation chart 15 years India example

PPF vs FD vs ELSS comparison table India infographic

Indian family long term savings planning PPF account

PPF account opening form India post office bank

For many Indian citizens, especially middle-class families, one question always comes up:

“Where can I invest safely for long term without worrying about market risk?”

One simple answer is:

👉 Public Provident Fund (PPF)

PPF is one of the safest long-term savings options in India. It is government-backed, tax-friendly, and disciplined.

In this article, we will explain PPF in India with proper calculation, in a simple, practical, and friendly way, using real Indian examples.

No complex formulas. Only clear understanding.

What Is PPF? (In Simple Words)

PPF (Public Provident Fund) is a long-term savings scheme launched by the Government of India.

It is:

✅ Safe

✅ Government-backed

✅ Tax-saving

✅ Long-term

✅ Low risk

It is ideal for people who want security more than high returns.

Who Controls PPF in India?

PPF is governed by the Government of India and follows rules notified by:

Ministry of Finance (India)

Interest rates are decided quarterly by the government.

PPF accounts can be opened in:

Post Offices

Nationalized Banks

Selected Private Banks

Key Features of PPF

| Feature | Details |

|---|---|

| Lock-in Period | 15 Years |

| Minimum Investment | ₹500 per year |

| Maximum Investment | ₹1.5 lakh per year |

| Interest Rate | Around 7–8% (changes quarterly) |

| Risk | Very Low |

| Tax Benefit | Yes (EEE) |

What Does EEE Mean?

PPF is an EEE (Exempt-Exempt-Exempt) investment.

It means:

1️⃣ Investment is tax deductible (Section 80C)

2️⃣ Interest earned is tax-free

3️⃣ Maturity amount is tax-free

This makes PPF very powerful for tax planning.

👉 Related Read:

Internal Link: ELSS Mutual Funds Explained

https://marketmeterab.blogspot.com/elss-mutual-funds-india

How PPF Interest Is Calculated

Interest in PPF is calculated:

👉 On lowest balance between 5th and last day of every month

👉 Compounded yearly

So, best practice:

💡 Invest before 5th of April to get full-year interest.

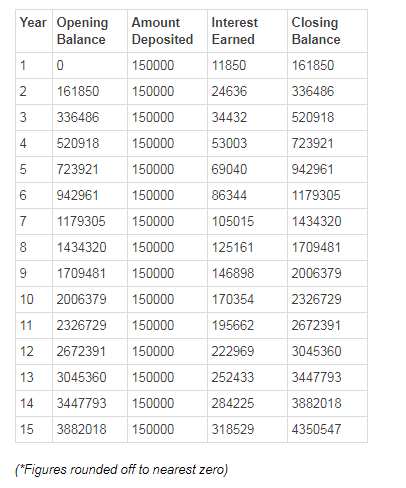

PPF Calculation Example (Very Important)

Let’s understand with real numbers.

Case 1: Monthly Investment ₹5,000

Monthly investment: ₹5,000

Yearly investment: ₹60,000

Duration: 15 years

Interest rate: 7.5% (example)

Total Invested:

₹60,000 × 15 = ₹9,00,000

Approx Maturity Value:

₹16–18 lakh

So, ₹9 lakh becomes nearly double.

Case 2: Maximum Investment ₹1.5 Lakh Per Year

Annual investment: ₹1,50,000

Duration: 15 years

Interest rate: 7.5%

Total Invested:

₹22,50,000

Approx Maturity Value:

₹40–45 lakh

This is fully tax-free.

Chart: PPF Growth Over 15 Years (₹1.5 Lakh Yearly)

Year 1: ₹1,50,000

Year 5: ₹8–9 lakh

Year 10: ₹18–20 lakh

Year 15: ₹40+ lakh

Compounding works silently.

Partial Withdrawal Rules

After 7 years:

👉 Partial withdrawal allowed.

Loan facility available from 3rd year.

This gives some flexibility.

Can You Extend PPF After 15 Years?

Yes.

You can:

1️⃣ Close account and withdraw

2️⃣ Extend with contribution

3️⃣ Extend without contribution

Many people extend for 5 more years.

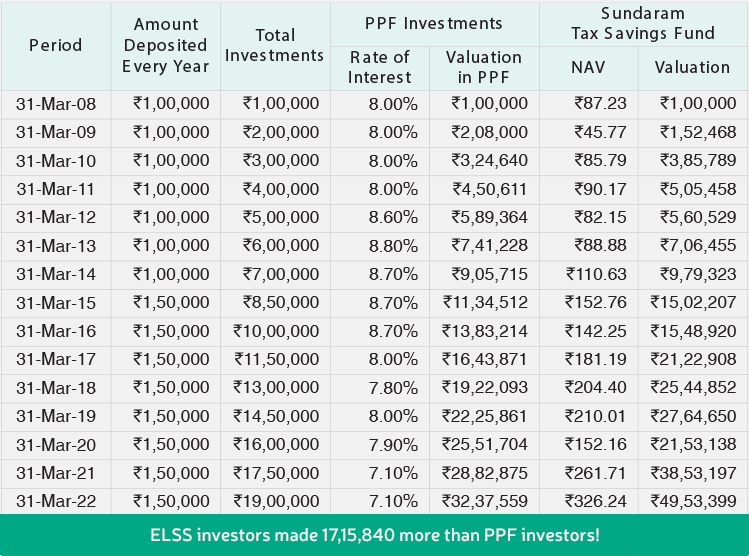

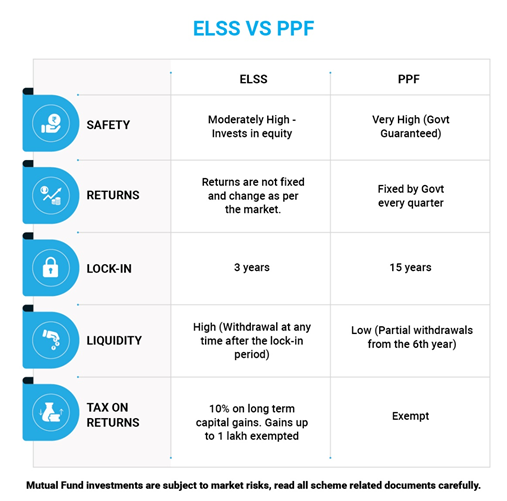

PPF vs FD vs ELSS (Comparison Table)

| Feature | PPF | FD | ELSS |

|---|---|---|---|

| Risk | Very Low | Low | Medium |

| Returns | 7–8% | 5–6% | 10–12% (long term) |

| Lock-in | 15 Years | 5 Years | 3 Years |

| Tax on Maturity | No | Yes | Yes (LTCG rules) |

| Suitable For | Safety Seekers | Conservative | Growth Seekers |

👉 PPF = Safety

👉 ELSS = Growth

Real-Life Indian Example

Case: Suman (School Teacher, Kolkata)

Age: 30

Invests ₹1 lakh yearly in PPF

At age 45:

Total invested: ₹15 lakh

Value: ₹28–30 lakh

Tax-free corpus.

This supports her child’s education.

Who Should Invest in PPF?

PPF is ideal for:

✅ Salaried employees

✅ Risk-averse investors

✅ Government employees

✅ People planning retirement

✅ Parents saving for children

Not ideal for:

❌ People seeking quick returns

❌ Traders

❌ Short-term investors

Best Strategy for Indian Citizens

Smart investors combine:

PPF for safety

SIP for growth

👉 Related Read:

Internal Link: Long Term vs Short Term Investing

https://marketmeterab.blogspot.com/long-term-vs-short-term-investing

When Should You Deposit in PPF?

Best time:

👉 Before 5th April each year

Why?

You earn interest for full year.

Small timing gives extra money.

PPF Account Opening Process

Steps:

1️⃣ Visit bank/post office

2️⃣ Fill PPF form

3️⃣ Submit PAN, Aadhaar

4️⃣ Deposit minimum ₹500

Many banks allow online opening.

👉 Related Read:

Internal Link: How to Open Demat Account in India

https://marketmeterab.blogspot.com/how-to-open-demat-account

(Understand difference between market and savings products.)

Common Mistakes Indians Make in PPF

Depositing after 5th date

Missing yearly minimum

Expecting stock-like returns

Ignoring extension option

Not using full ₹1.5 lakh limit

Avoid these.

PPF and Retirement Planning

PPF works well for:

Conservative retirement planning

Safe long-term accumulation

Backup corpus

But inflation may reduce real value.

So combine with growth investments.

PPF vs Stock Market Returns

| Feature | PPF | Stock Market |

|---|---|---|

| Risk | Very Low | Medium |

| Return | Moderate | Higher |

| Volatility | None | High |

| Peace of Mind | High | Depends |

👉 Balance both for best results.

Statutory Disclaimer

PPF interest rates are subject to change as notified by the Government of India. This article is for educational purposes only and does not constitute financial advice. Investors should evaluate their financial goals and consult a qualified advisor before making investment decisions. Market-linked products are regulated by Securities and Exchange Board of India, while PPF is governed by the Government of India.

Frequently Asked Questions (FAQ)

Q1. Is PPF 100% safe?

Yes, backed by Government of India.

Q2. Can I withdraw before 15 years?

Partial withdrawal allowed after 7 years.

Q3. Can I invest monthly?

Yes, monthly or yearly.

Q4. Is PPF better than FD?

For long-term tax-free growth, yes.

Q5. Can husband and wife both open PPF?

Yes, separate accounts allowed.

Useful Video & Image Resources

PPF Explained in Hindi:

https://www.youtube.com/watch?v=F8M2Q9L7X4APPF Calculation Example:

https://www.youtube.com/watch?v=K9F3L2M8X7QIndia Post PPF Details:

https://www.indiapost.gov.inSBI PPF Information:

https://sbi.co.in

Bibliography

Ministry of Finance (India) Notifications

RBI Financial Stability Reports

Income Tax Act – Section 80C

Bank PPF Brochures

Government Savings Scheme Guidelines

Suggested Internal Links for MarketMeterAB

What Is Stock Market in India

https://marketmeterab.blogspot.com/what-is-stock-market-indiaELSS Mutual Funds Explained

https://marketmeterab.blogspot.com/elss-mutual-funds-indiaSIP vs Lump Sum Investment

https://marketmeterab.blogspot.com/sip-vs-lumpsumLong Term vs Short Term Investing

https://marketmeterab.blogspot.com/long-term-vs-short-term-investingCharges in Stock Trading Explained

https://marketmeterab.blogspot.com/stock-trading-charges-india

Final Words

PPF is not for fast money.

It is for:

✅ Stability

✅ Discipline

✅ Tax savings

✅ Long-term security

If you want peace of mind and safe growth, PPF is a strong option.

But remember:

👉 Safety builds foundation.

👉 Growth builds wealth.

Combine both wisely, and your financial future will stay strong and balanced.

Comments

Post a Comment