Senior Citizen Saving Scheme in India Explained: Interest, Benefits & Calculation (2026 Guide)

Senior Citizen Saving Scheme in India Explained: Safe Income Guide for Retirement

Senior Citizen Saving Scheme in India Explained: Interest, Benefits & Calculation (2026 Guide)

Learn how the Senior Citizen Saving Scheme (SCSS) works in India. Understand interest rate, tax benefits, eligibility, calculation, and monthly income with simple examples.

Senior Citizen Saving Scheme passbook India post office example

SCSS account opening form post office bank India

Senior citizen savings planning India government scheme

SCSS quarterly interest payout chart India infographic

Indian senior citizen checking savings account passbook

After retirement, most Indian citizens want only three things:

✔ Regular income

✔ Safety of money

✔ Peace of mind

But bank FD rates are falling, and market investments feel risky at old age.

That is why the government introduced a special scheme:

👉 Senior Citizen Saving Scheme (SCSS)

In this article, we will explain Senior Citizen Saving Scheme in India in a simple, practical, and friendly way, using real Indian examples.

No complicated finance words. Only clear guidance.

What Is Senior Citizen Saving Scheme? (Simple Meaning)

Senior Citizen Saving Scheme (SCSS) is a government-backed savings scheme specially for senior citizens.

Its main purpose is:

✅ Give regular income

✅ Protect retirement savings

✅ Provide higher interest than FD

✅ Offer tax benefits

In short:

👉 SCSS = Pension-like income + Full safety

Who Runs SCSS in India?

SCSS is governed by the Government of India under:

👉 Ministry of Finance (India)

Accounts are opened through:

Authorized Banks (SBI, PNB, BOI, etc.)

So, it is fully government-supported.

Who Can Open SCSS Account?

You can open SCSS if:

✅ Age is 60 years or above

✅ Age is 55–60 (retired under VRS/superannuation)

✅ You are an Indian resident

NRIs and HUFs are not allowed.

Key Features of Senior Citizen Saving Scheme

| Feature | Details |

|---|---|

| Scheme Type | Government Savings |

| Eligibility | 60+ Years |

| Lock-in Period | 5 Years |

| Extension | 3 Years |

| Min Deposit | ₹1,000 |

| Max Deposit | ₹30 Lakh |

| Interest Rate | Around 8%+ (Varies) |

| Risk | Very Low |

| Payout | Quarterly |

SCSS offers one of the highest safe interest rates in India.

How SCSS Interest Is Paid

Interest is:

👉 Calculated yearly

👉 Paid every 3 months

👉 Directly credited to bank account

Payout Months:

April

July

October

January

So, you get income four times a year.

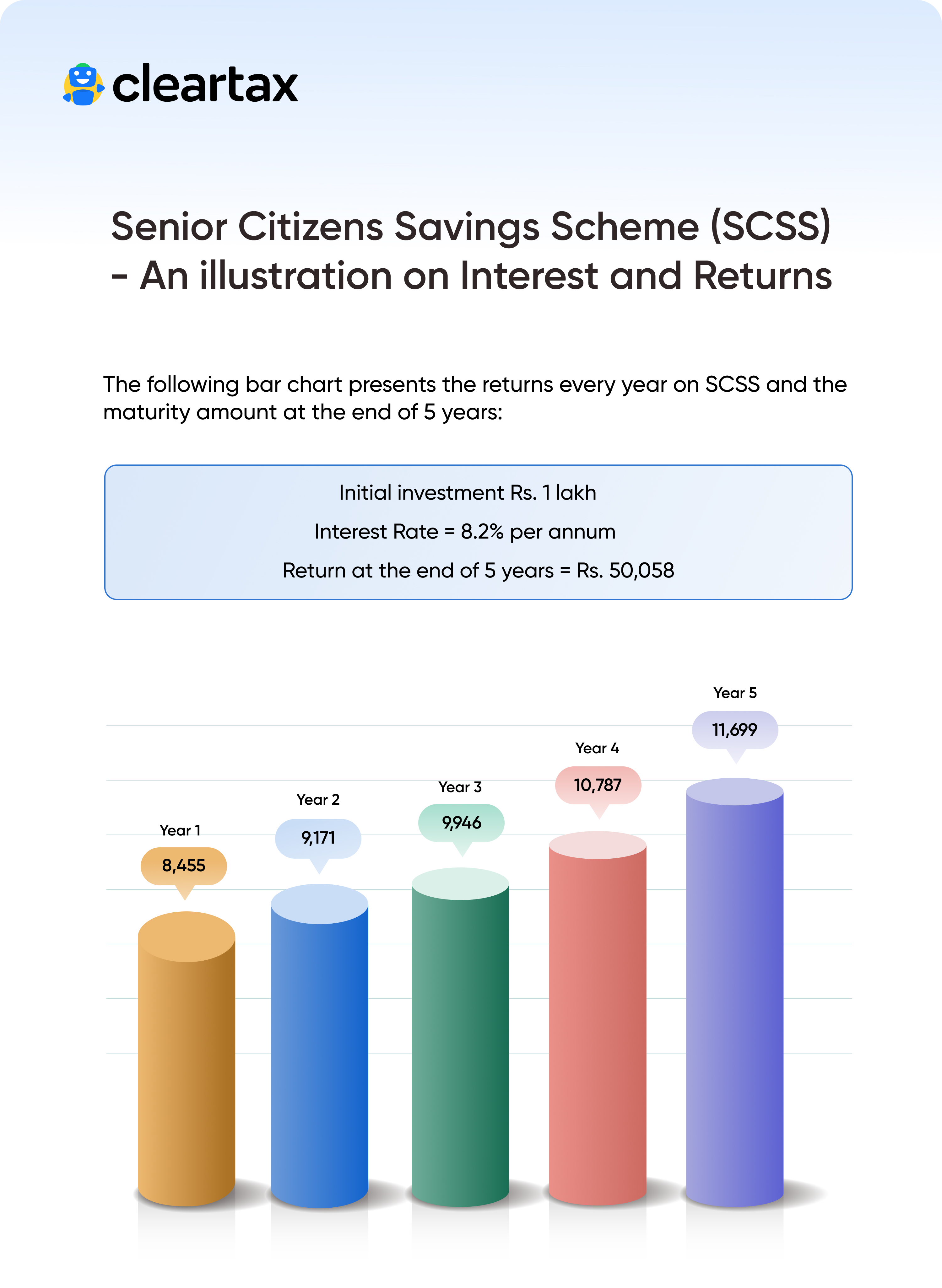

How SCSS Interest Is Calculated

Interest is simple interest, not compound.

Formula:

👉 Interest = Deposit × Rate × Time

It is paid quarterly.

Calculation Example (Very Important)

Let us understand with real numbers.

Case 1: Deposit ₹10 Lakh

Investment: ₹10,00,000

Interest Rate: 8.2% (example)

Yearly Interest:

₹82,000

Quarterly Income:

₹20,500

So, every 3 months you get:

👉 ₹20,500

Case 2: Maximum Deposit ₹30 Lakh

Investment: ₹30,00,000

Interest: 8.2%

Yearly Income:

₹2,46,000

Quarterly Income:

₹61,500

This is like monthly pension.

Chart: SCSS Income Flow

Deposit Money

↓

Government Pays Interest

↓

Quarterly Bank Credit

↓

Regular Income

Simple and reliable.

Real-Life Indian Example

Case: Shyamlal (Retired Clerk, Gaya)

Age: 62

Retirement money: ₹15 lakh

Invested ₹12 lakh in SCSS

Income:

Quarterly = ₹24,600 (approx)

Yearly = ₹98,000+

This helps in:

✔ Medicines

✔ Groceries

✔ Electricity bills

Without touching capital.

Lock-in and Extension Rules

Initial Period: 5 Years

You cannot withdraw fully before 5 years (penalty applies).

Extension: 3 Years

After 5 years, you can extend for 3 more years.

This gives total:

👉 Up to 8 years.

Premature Withdrawal Rules

| Period | Penalty |

|---|---|

| Before 1 Year | Not Allowed |

| 1–2 Years | 1.5% |

| After 2 Years | 1% |

So, SCSS is best for long-term retirees.

Tax Benefits in SCSS

SCSS comes under:

Benefit:

Investment up to ₹1.5 lakh = Tax Deduction

But remember:

❌ Interest is taxable

❌ TDS applies if interest > ₹50,000/year

👉 Related Read:

Internal Link: Mutual Fund Taxation in India

https://marketmeterab.blogspot.com/mutual-fund-taxation-india

SCSS vs FD vs PPF vs NPS

| Feature | SCSS | FD | PPF | NPS |

|---|---|---|---|---|

| Risk | Very Low | Low | Very Low | Medium |

| Returns | High (Safe) | Medium | Medium | High |

| Income | Regular | Optional | No | Pension |

| Lock-in | 5 Years | Flexible | 15 Years | Till 60 |

| Best For | Retirees | All | Long Term | Retirement |

👉 SCSS is best for retired people who need income.

How to Open SCSS Account

You can open SCSS in:

✅ Post Office

✅ Selected Banks

Documents Required

Aadhaar Card

PAN Card

Age Proof

Passport Size Photo

Retirement Proof (if below 60)

Steps

1️⃣ Visit bank/post office

2️⃣ Fill SCSS form

3️⃣ Submit documents

4️⃣ Deposit money

5️⃣ Get passbook

Some banks also allow online application.

Best Strategy for Senior Citizens

Smart retirees combine:

SCSS for income

FD for emergency

Mutual Funds (small part) for growth

Example:

| Tool | % |

|---|---|

| SCSS | 50% |

| FD | 30% |

| Mutual Fund | 20% |

This gives balance.

👉 Related Read:

Internal Link: Long Term vs Short Term Investing

https://marketmeterab.blogspot.com/long-term-vs-short-term-investing

SCSS and Stock Market

Senior citizens should be careful with markets.

If interested, start small.

👉 Related Read:

Internal Link: What Is Stock Market in India

https://marketmeterab.blogspot.com/what-is-stock-market-india

Common Mistakes Indians Make in SCSS

Not nominating family member

Ignoring tax on interest

Withdrawing early

Putting all money in one scheme

Not extending after 5 years

Avoid these mistakes.

Nomination Facility in SCSS

You can nominate:

✅ Spouse

✅ Son/Daughter

✅ Any family member

This avoids future legal trouble.

Always fill nomination.

Safety of Senior Citizen Saving Scheme

SCSS is backed by Government of India.

So:

✔ No market risk

✔ No company risk

✔ No default risk

It is one of the safest schemes.

Role of Market Regulator

Market-linked products are regulated by:

👉 Securities and Exchange Board of India

SCSS is outside market risk.

That is why it suits senior citizens.

Statutory Disclaimer

Senior Citizen Saving Scheme interest rates, rules, and tax benefits are subject to change as per Government of India notifications. This article is for educational purposes only and does not constitute financial advice. Investors should evaluate their financial needs and consult a qualified advisor before investing.

Frequently Asked Questions (FAQ)

Q1. Is SCSS better than FD?

For senior citizens, yes. It gives higher safe returns.

Q2. Can husband and wife both open SCSS?

Yes. Both can invest separately.

Q3. Is interest monthly?

No. It is paid quarterly.

Q4. Can I invest more than ₹30 lakh?

No. ₹30 lakh is the maximum limit.

Q5. What happens after 5 years?

You can extend for 3 more years or withdraw.

Useful Video & Image Resources

SCSS Explained in Hindi:

https://www.youtube.com/watch?v=F8M2Q9L7X4ASenior Citizen Investment Guide:

https://www.youtube.com/watch?v=K9F3L2M8X7QIndia Post SCSS Info:

https://www.indiapost.gov.inSBI SCSS Page:

https://sbi.co.in

Bibliography

Ministry of Finance Notifications

Government Savings Scheme Guidelines

Income Tax Act – Section 80C

RBI Financial Stability Reports

Bank & Post Office SCSS Brochures

Suggested Internal Links for MarketMeterAB

EPF vs PPF Difference Explained

https://marketmeterab.blogspot.com/epf-vs-ppf-differencePPF in India Explained

https://marketmeterab.blogspot.com/ppf-india-explainedNPS Scheme in India Explained

https://marketmeterab.blogspot.com/nps-scheme-indiaHow Dividends Work in India

https://marketmeterab.blogspot.com/how-dividends-workCharges in Stock Trading Explained

https://marketmeterab.blogspot.com/stock-trading-charges-india

Final Words

Senior Citizen Saving Scheme is like a strong walking stick in old age.

It gives:

✅ Regular income

✅ Full safety

✅ Government guarantee

✅ Mental peace

If you or your parents are retired, SCSS should be part of your financial plan.

👉 Remember: In retirement, safety and steady income matter more than fast growth. Choose wisely.

Comments

Post a Comment