SIP vs Lump Sum Investment in India: Which is Better for Middle-Class Investors?

SIP vs Lump Sum Investment in India: Which is Better for Middle-Class Investors?

For most Indian middle-class and working citizens, investing money is not about becoming rich overnight. It is about financial safety, future security, and peaceful sleep. When people start learning about mutual funds, one question always comes first:

“Should I invest through SIP or Lump Sum in India?”

This confusion is very common, especially among salaried employees, small business owners, and self-employed professionals.

This article explains SIP vs Lump Sum investment in India in a simple, practical, and real-life Indian way, without complicated financial words.

What is SIP Investment? (Simple Meaning)

SIP (Systematic Investment Plan) means investing a fixed amount every month into a mutual fund.

Example:

You invest ₹3,000 every month

Money is invested automatically

You buy more units when market is down

You buy fewer units when market is high

This process reduces risk and builds discipline.

👉 Beginner-friendly guide:

Internal Link: What is SIP and How SIP Works in India

https://marketmeterab.blogspot.com/what-is-sip-india

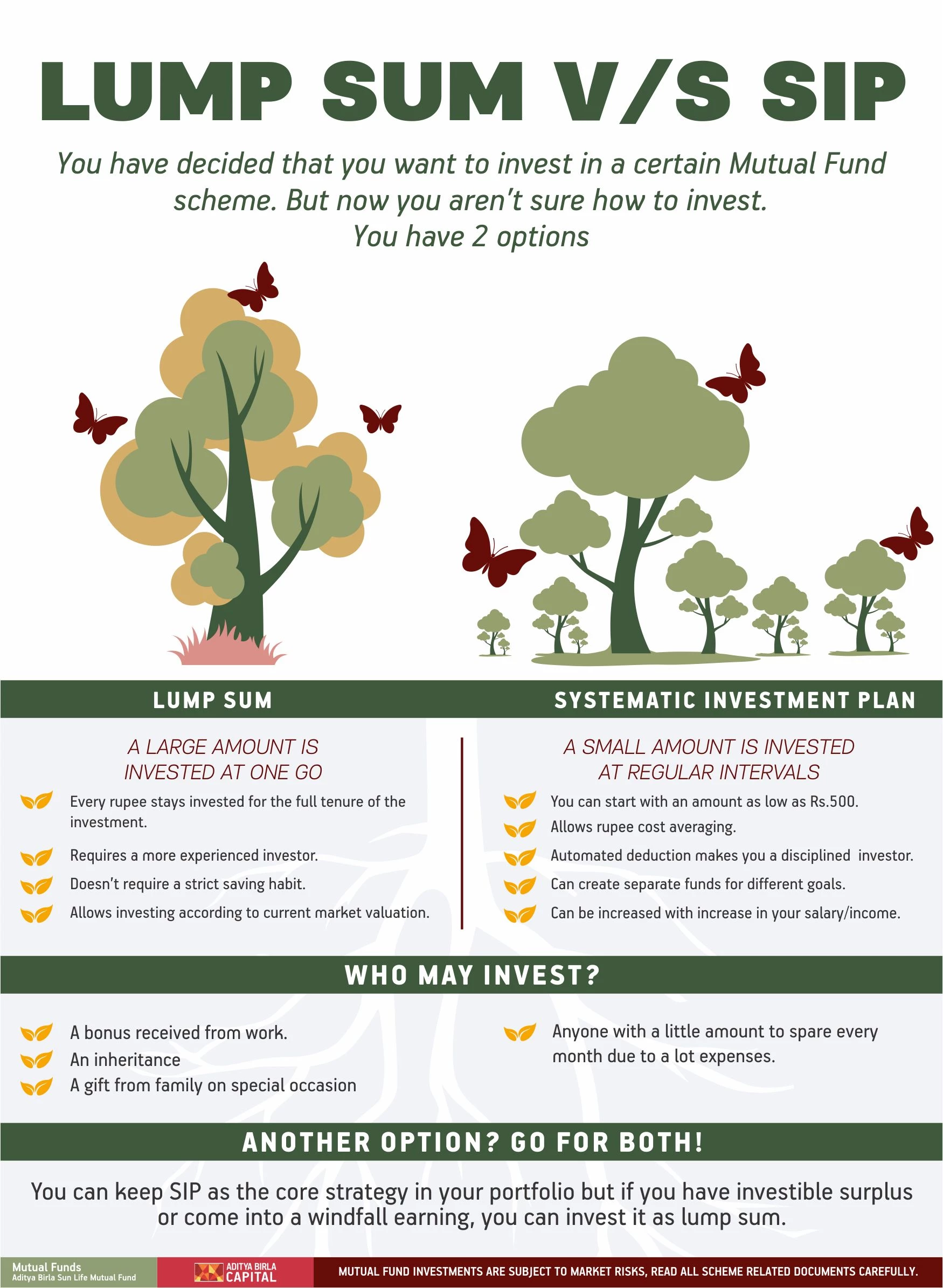

What is Lump Sum Investment?

Lump sum investment means investing a large amount at one time.

Example:

You invest ₹1,00,000 at once

Market movement immediately affects your investment

Returns depend heavily on timing

This method suits people who have surplus money ready.

SIP vs Lump Sum: Basic Difference Table

| Feature | SIP | Lump Sum |

|---|---|---|

| Investment Style | Monthly small amount | One-time large amount |

| Best For | Salaried & middle class | People with surplus funds |

| Market Timing Needed | No | Yes |

| Risk Level | Lower (long-term) | Higher (short-term) |

| Discipline | Automatic | Manual |

| Stress Level | Low | High |

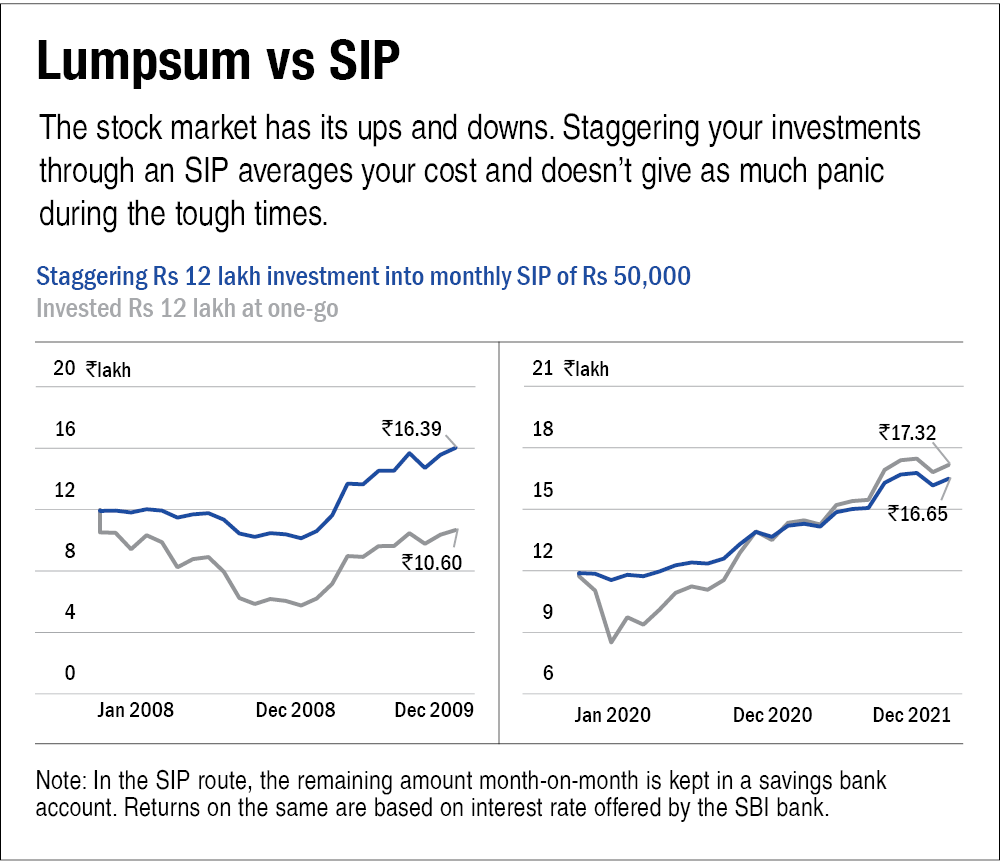

SIP vs Lump Sum: Indian Example (Very Important)

Case 1: SIP Investor – Amit (Office Employee)

Monthly SIP: ₹5,000

Investment period: 15 years

Total invested: ₹9,00,000

Estimated value @12% return: ₹25–27 lakh

Amit did not worry about market ups and downs.

Case 2: Lump Sum Investor – Raj (Business Owner)

One-time investment: ₹9,00,000

Invested when market was high

Market fell 20% after investment

Result:

Portfolio value dropped sharply

Emotional stress increased

Panic selling risk increased

👉 This is where SIP wins for common Indians.

How SIP Reduces Risk: Rupee Cost Averaging

SIP follows a concept called Rupee Cost Averaging.

| Market Level | Units Purchased |

|---|---|

| Market High | Fewer units |

| Market Low | More units |

Over time, average cost becomes lower.

Lump sum investment does not get this benefit.

Which is Better During Market Volatility?

| Situation | SIP | Lump Sum |

|---|---|---|

| Market Falling | Very Good | Risky |

| Market Rising | Good | Good |

| Market Uncertain | Best | Dangerous |

👉 Indian markets are volatile. SIP suits Indian conditions better.

SIP vs Lump Sum for Indian Salaried Class

SIP is Better Because:

Salary comes monthly

Expenses are regular

No pressure of timing

Easy budgeting

Lump Sum is Difficult Because:

Rarely have big idle money

Emotional decisions increase

Requires market knowledge

When Lump Sum Investment Makes Sense in India

Lump sum investment is useful when:

You receive bonus or inheritance

Market has corrected heavily

You have long-term horizon (10+ years)

You understand market cycles

Even then, many experts suggest Systematic Transfer Plan (STP) instead of direct lump sum.

👉 Read more:

Internal Link: STP Explained for Indian Investors

https://marketmeterab.blogspot.com/stp-mutual-fund-india

SIP vs Lump Sum Returns: Long-Term Reality

Over long periods (15–20 years):

SIP returns and Lump Sum returns tend to be similar

SIP wins emotionally and behaviorally

Lump sum requires perfect timing (very rare)

👉 Discipline beats intelligence in investing.

Taxation: SIP vs Lump Sum in India

There is no difference in tax rules.

Equity mutual funds taxed as per holding period

Long-term capital gains above ₹1.25 lakh are taxable

SIP is treated as multiple investments with different dates

Common Mistakes Indians Make

Stopping SIP during market fall

Investing lump sum after market rallies

Copying others without understanding

Expecting quick returns

Ignoring emergency fund

👉 First build emergency fund, then invest.

SIP + Lump Sum: Best Indian Strategy

Smart Indian investors use both:

SIP for regular income

Lump sum during market corrections

SIP step-up with salary hikes

This balanced approach works best.

Statutory Disclaimer

Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully. Past performance is not indicative of future returns. This article is for educational purposes only and not investment advice. Please invest based on your risk profile and financial goals as guided by regulations issued by SEBI.

Frequently Asked Questions (FAQ)

Q1. Is SIP safer than lump sum?

Yes, SIP reduces risk through time averaging.

Q2. Can I convert lump sum into SIP?

Yes, via Systematic Transfer Plan (STP).

Q3. Which gives higher returns?

Both give similar returns long term. SIP wins emotionally.

Q4. Is lump sum bad?

No, but it requires correct timing and patience.

Q5. Should beginners avoid lump sum?

Beginners should prefer SIP.

Useful Videos & Images

SIP vs Lump Sum Explained (Hindi):

https://www.youtube.com/watch?v=V5F7k4G0P0kRupee Cost Averaging Explained:

https://www.youtube.com/watch?v=8eY2xP5M0mYSIP vs Lump Sum Chart:

https://www.amfiindia.com/images/sip-vs-lumpsum.png

Bibliography

AMFI India – Investor Education

SEBI Mutual Fund Guidelines

Historical Nifty 50 Data

Mutual Fund Offer Documents

Suggested Internal Links for further studies :

Best SIP Amount for Beginners in India

https://marketmeterab.blogspot.com/best-sip-amount-indiaBest Mutual Funds for Long Term Wealth

https://marketmeterab.blogspot.com/best-mutual-funds-indiaHow Indians Can Build Wealth Slowly

https://marketmeterab.blogspot.com/wealth-building-india

Final Words

For Indian middle-class investors, SIP is peace, and lump sum is opportunity.

If you want stress-free wealth creation, SIP is your best friend.

If you get extra money and understand markets, lump sum can help.

👉 Consistency matters more than amount or timing.

This simple truth has built wealth for millions of Indians.

{kind=link}

Comments

Post a Comment