Sukanya Samriddhi Yojana in India Explained: Interest, Benefits & Calculation (2026 Guide)

Sukanya Samriddhi Yojana in India Explained: Complete Guide for Parents

Sukanya Samriddhi Yojana in India Explained: Interest, Benefits & Calculation (2026 Guide)

Learn how Sukanya Samriddhi Yojana works in India with simple examples, interest rate, tax benefits, maturity rules, and return calculation for girl child savings.

Sukanya Samriddhi Yojana passbook India savings example

SSY account opening form post office bank India

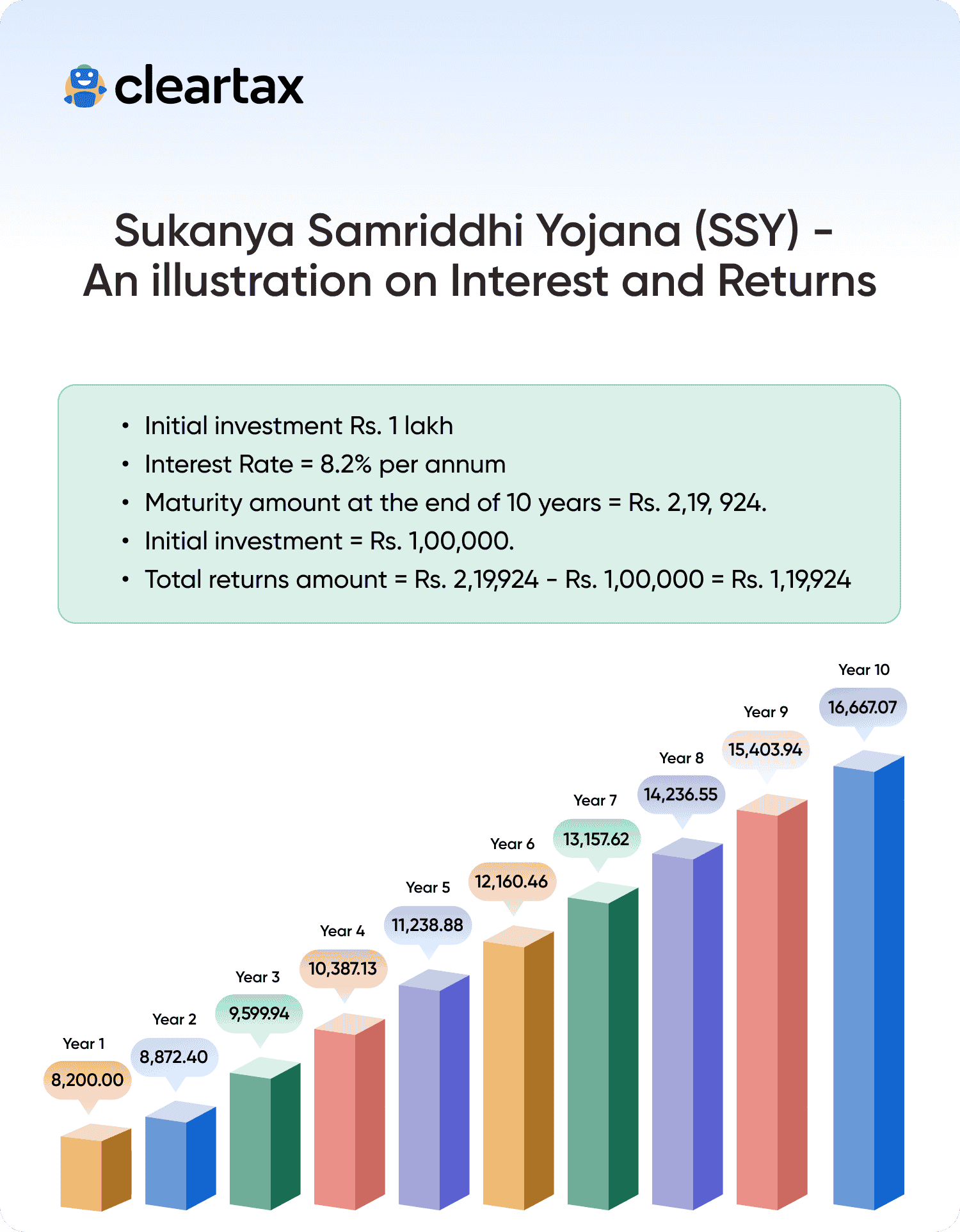

Sukanya Samriddhi Yojana interest calculation chart 21 years

Indian parents saving for girl child education SSY scheme

Sukanya Samriddhi deposit receipt bank post office India

For most Indian parents, one dream is common:

“I want to give my daughter the best education and a secure future.”

But rising education fees and marriage expenses worry many families.

This is where a powerful government scheme helps:

👉 Sukanya Samriddhi Yojana (SSY)

In this article, we will explain Sukanya Samriddhi Yojana in India in a simple, practical, and friendly way, using real-life Indian examples.

No difficult finance terms. Only clear understanding.

What Is Sukanya Samriddhi Yojana? (Simple Meaning)

Sukanya Samriddhi Yojana (SSY) is a savings scheme specially for girl children.

It was launched under the “Beti Bachao, Beti Padhao” initiative and is governed by:

👉 Ministry of Finance (India)

The main purpose is:

✅ Support girl child education

✅ Help in marriage expenses

✅ Encourage long-term savings

✅ Provide high, safe returns

In short:

👉 SSY = Future security for daughters

Who Can Open Sukanya Samriddhi Account?

SSY can be opened for:

Girl child below 10 years of age

By parents or legal guardians

Maximum two accounts per family (generally)

Only Indian resident girls are eligible.

Key Features of Sukanya Samriddhi Yojana

| Feature | Details |

|---|---|

| Scheme Type | Government-backed savings |

| Beneficiary | Girl child |

| Lock-in Period | 21 Years |

| Deposit Period | First 15 Years |

| Min Deposit | ₹250 per year |

| Max Deposit | ₹1.5 lakh per year |

| Risk | Very Low |

| Tax Benefit | EEE (Tax-Free) |

SSY is one of the safest schemes in India.

What Does EEE Benefit Mean?

SSY follows EEE (Exempt-Exempt-Exempt) rule:

1️⃣ Investment → Tax-free (80C)

2️⃣ Interest → Tax-free

3️⃣ Maturity → Tax-free

So, you don’t pay any tax at any stage.

This is a big advantage.

👉 Related Read:

Internal Link: PPF in India Explained with Calculation

https://marketmeterab.blogspot.com/ppf-india-explained

How Sukanya Samriddhi Interest Is Calculated

Interest is:

👉 Calculated monthly

👉 Compounded yearly

👉 Declared quarterly by government

Current rates are usually between 7.5% – 8.5% (varies with time).

Best practice:

💡 Deposit before 5th of every month for full interest.

How Long Do You Need to Invest?

SSY works in two phases:

Phase 1: Deposit Period (15 Years)

You invest yearly for 15 years.

Phase 2: Maturity Period (Next 6 Years)

No deposit needed. Money grows automatically.

Total duration = 21 Years

Calculation Example: Sukanya Samriddhi Returns

Let’s understand with real numbers.

Case 1: ₹50,000 Per Year Investment

Annual Deposit: ₹50,000

Deposit Period: 15 Years

Total Invested: ₹7.5 lakh

Interest: 8% (example)

Approx Maturity Value:

👉 ₹22–25 lakh

₹7.5 lakh becomes 3 times.

Case 2: Maximum ₹1.5 Lakh Per Year

Annual Deposit: ₹1,50,000

Deposit Period: 15 Years

Total Invested: ₹22.5 lakh

Approx Maturity Value:

👉 ₹65–70 lakh

Completely tax-free.

Chart: SSY Growth Example (₹1.5 Lakh/Year)

Year 5 → ₹9–10 lakh

Year 10 → ₹22–25 lakh

Year 15 → ₹40–45 lakh

Year 21 → ₹65+ lakh

Time + discipline = big wealth.

Real-Life Indian Example

Case: Rina (Homemaker, Patna)

Opened SSY for daughter at age 2

Invests ₹60,000/year

At daughter’s age 23:

Total Invested: ₹9 lakh

Value: ₹28+ lakh

This helps in college + marriage.

That is smart planning.

Withdrawal Rules in Sukanya Samriddhi

For Education (After Age 18)

For higher studies

For Marriage (After 18 Years)

Full withdrawal allowed

At Maturity (21 Years)

Full amount can be withdrawn

So, money is available when needed most.

How to Open SSY Account in India

You can open SSY account in:

✅ Post Office

✅ SBI, PNB, BOI, and other banks

✅ Selected private banks

Documents Required

Girl child birth certificate

Parent’s Aadhaar & PAN

Address proof

Photos

Process is simple and mostly offline (some banks offer online).

Sukanya Samriddhi vs PPF vs NPS

| Feature | SSY | PPF | NPS |

|---|---|---|---|

| Beneficiary | Girl Child | All | All |

| Lock-in | 21 Years | 15 Years | Till 60 |

| Risk | Very Low | Very Low | Medium |

| Returns | High (Govt) | Medium | High |

| Pension | No | No | Yes |

SSY is best for girl child planning.

👉 Related Read:

Internal Link: EPF vs PPF Difference Explained

https://marketmeterab.blogspot.com/epf-vs-ppf-difference

Who Should Invest in SSY?

SSY is ideal for:

✅ Parents of young daughters

✅ Middle-class families

✅ Risk-averse investors

✅ Long-term planners

✅ Tax savers

Not suitable for:

❌ Parents of boys only

❌ Short-term investors

❌ Those needing liquidity

Best Strategy for Indian Parents

Smart parents combine:

SSY for daughter

SIP for growth

PPF for safety

Example Plan

| Tool | Purpose |

|---|---|

| SSY | Daughter’s future |

| SIP | Wealth growth |

| PPF | Safety backup |

This builds balanced security.

👉 Related Read:

Internal Link: Best SIP Amount for Beginners

https://marketmeterab.blogspot.com/best-sip-amount-india

Common Mistakes Indians Make in SSY

Missing yearly deposit

Depositing after deadline

Closing early

Not using full limit

No backup investment

Avoid these for best results.

Sukanya Samriddhi and Tax Planning

SSY helps in:

✅ Section 80C deduction (₹1.5 lakh)

✅ No tax on interest

✅ No tax on maturity

Learn more:

Internal Link: Mutual Fund Taxation in India

https://marketmeterab.blogspot.com/mutual-fund-taxation-india

Safety and Guarantee of SSY

SSY is backed by Government of India.

So:

✔ No market risk

✔ No company risk

✔ No default risk

It is among the safest schemes.

Statutory Disclaimer

Sukanya Samriddhi Yojana interest rates, rules, and tax benefits are subject to change as per Government of India notifications. This article is for educational purposes only and does not constitute financial advice. Investors should evaluate their financial goals and consult a qualified advisor before making decisions.

Frequently Asked Questions (FAQ)

Q1. Can I open SSY for two daughters?

Yes, usually two accounts per family are allowed.

Q2. Is SSY better than FD?

For long-term and tax-free returns, yes.

Q3. Can grandparents open SSY?

Only if they are legal guardians.

Q4. What if I miss deposit?

Small penalty applies, but account can be revived.

Q5. Can I close SSY early?

Only in special cases like medical emergency.

Useful Video & Image Resources

SSY Explained in Hindi:

https://www.youtube.com/watch?v=F8M2Q9L7X4ASukanya Samriddhi Calculation Guide:

https://www.youtube.com/watch?v=K9F3L2M8X7QSBI Sukanya Scheme Page:

https://sbi.co.in

Bibliography

Ministry of Finance Notifications

Government Savings Scheme Guidelines

Income Tax Act – Section 80C

RBI Financial Stability Reports

Bank and Post Office SSY Brochures

Suggested Internal Links for MarketMeterAB

NPS Scheme in India Explained

https://marketmeterab.blogspot.com/nps-scheme-indiaPPF in India Explained

https://marketmeterab.blogspot.com/ppf-india-explainedLong Term vs Short Term Investing

https://marketmeterab.blogspot.com/long-term-vs-short-term-investingHow to Open Demat Account

https://marketmeterab.blogspot.com/how-to-open-demat-accountHow Dividends Work in India

https://marketmeterab.blogspot.com/how-dividends-work

Final Words

Sukanya Samriddhi Yojana is not just a scheme.

It is:

✅ A promise for your daughter

✅ A shield against future expenses

✅ A gift of financial freedom

If you start early and stay regular, SSY can easily fund:

🎓 Higher education

💍 Marriage

🏡 Independence

👉 Remember: Strong daughters come from strong planning. Start today.

Comments

Post a Comment