What Is Term Insurance in India? Simple Guide to Life Cover & Family Security (2026)

What Is Term Insurance in India Explained: Complete Guide for Financial Protection

What Is Term Insurance in India? Simple Guide to Life Cover & Family Security (2026)

Learn what term insurance is in India, how it works, premium calculation, benefits, tax savings, and real examples. Beginner-friendly guide for family protection.

Term insurance policy India family financial protection concept

Indian family life insurance planning illustration

Term insurance comparison chart India infographic

Buying term life insurance online India laptop mobile

Life insurance advisor explaining term plan to Indian family

For most Indian families, one big worry is always there:

“What will happen to my family if something happens to me?”

If you are the main earning member, this question is very important.

The simplest and cheapest solution is:

👉 Term Insurance

In this article, we will explain what term insurance is in India in a simple, practical, and friendly way, using real Indian examples.

No complicated insurance language. Only clear understanding.

What Is Term Insurance? (In Simple Words)

Term insurance is a pure life insurance plan.

It means:

👉 You pay a small amount every year (premium).

👉 If you die during the policy period, your family gets money.

👉 If you survive, you get nothing.

So:

Term insurance = Protection, not investment

Its main job is:

✅ Secure your family’s future

✅ Replace your income

✅ Pay loans and expenses

Who Regulates Insurance in India?

All insurance companies in India are regulated by:

👉 Insurance Regulatory and Development Authority of India (IRDAI)

This body protects customers and ensures fair practices.

So, your term policy is safe and legally protected.

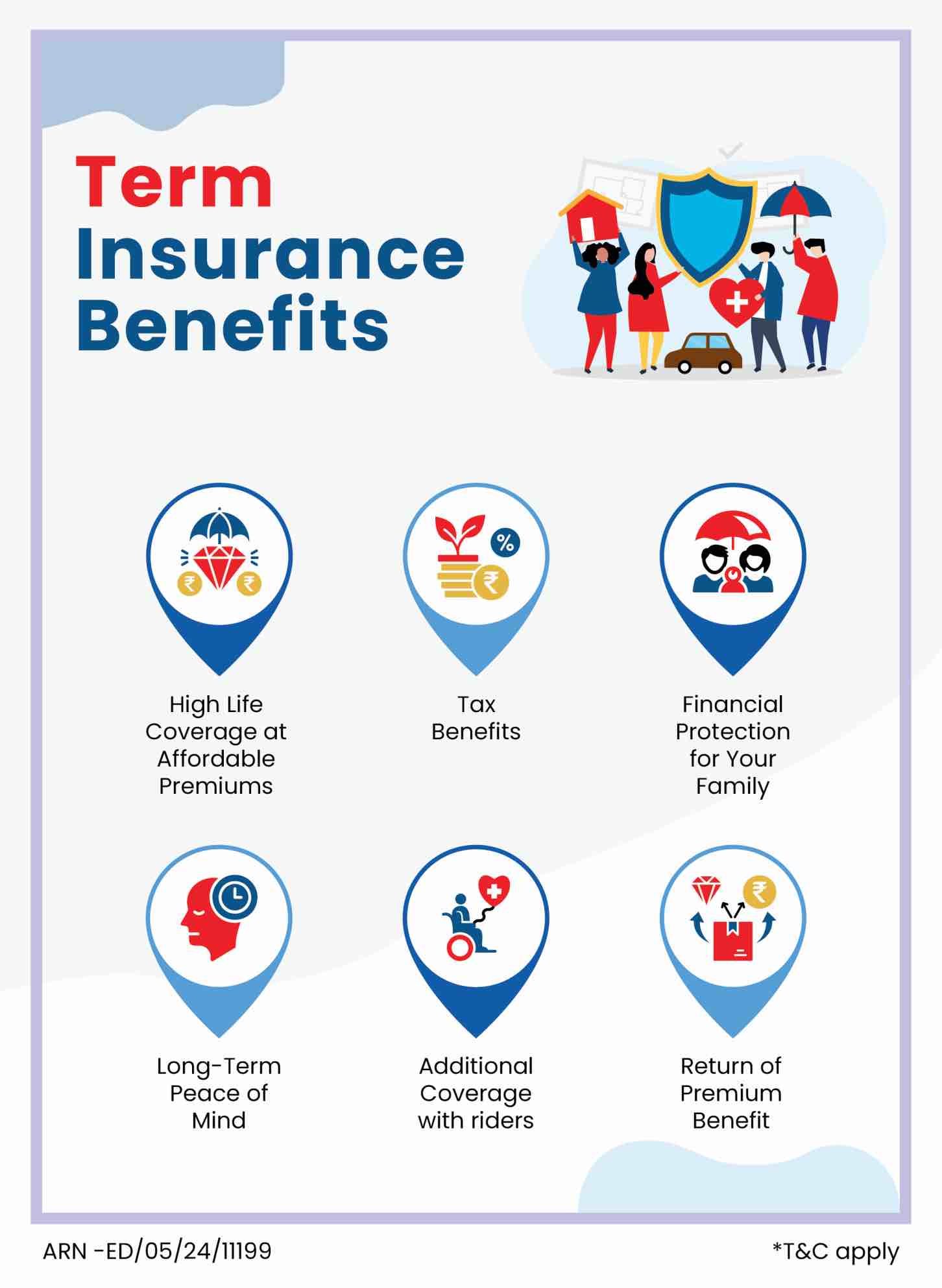

Why Term Insurance Is Important for Indians

Many Indians think:

“I have savings, FD, and some property. Is insurance needed?”

Yes. Because:

✔ Savings may not be enough

✔ Loans remain after death

✔ Children need education

✔ Spouse needs income

Term insurance gives big cover at low cost.

Real-Life Example (Very Common Case)

Case: Ramesh (Office Employee, Ranchi)

Age: 30

Salary: ₹35,000/month

Home Loan: ₹25 lakh

Two children

He buys:

👉 Term Plan: ₹1 crore cover

👉 Premium: ₹8,000/year

If something happens to Ramesh:

✔ Family gets ₹1 crore

✔ Loan cleared

✔ Children’s future safe

This is why term insurance matters.

How Term Insurance Works

Let us understand step-by-step.

Step 1: Choose Cover Amount

You decide how much money your family needs.

Example: ₹50 lakh / ₹1 crore / ₹2 crore

Step 2: Choose Policy Term

You choose how long you want coverage.

Example: Till age 60 or 65.

Step 3: Pay Premium

You pay monthly/yearly premium.

Example: ₹600 per month.

Step 4: Claim (If Death Happens)

If policyholder dies:

👉 Family gets full amount.

No deduction.

Chart: Term Insurance Working Flow

Buy Policy

↓

Pay Premium

↓

Policy Active

↓

(If Death)

↓

Family Gets Money

Simple and transparent.

Types of Term Insurance in India

There are mainly four types.

1️⃣ Level Term Plan (Most Popular)

Same cover throughout

Same premium

Best for most people.

2️⃣ Increasing Term Plan

Cover increases over time

Premium slightly higher

Good for inflation protection.

3️⃣ Decreasing Term Plan

Cover reduces with loan

Used for home loans

Good for borrowers.

4️⃣ Return of Premium Plan

Premium returned if you survive

Cost is very high

Usually not recommended.

How Much Term Insurance Do You Need?

Simple Rule:

👉 Cover = 15–20 × Annual Income

Example

Monthly Salary = ₹40,000

Annual = ₹4.8 lakh

Ideal Cover:

₹4.8L × 15 = ₹72 lakh

₹4.8L × 20 = ₹96 lakh

So, ₹75L – ₹1Cr is good.

Term Insurance Premium Example

Premium depends on:

✔ Age

✔ Health

✔ Smoking habit

✔ Cover amount

✔ Policy term

Sample Premium (Approx)

| Age | Cover | Yearly Premium |

|---|---|---|

| 25 | ₹1 Cr | ₹5,000–6,000 |

| 30 | ₹1 Cr | ₹7,000–9,000 |

| 35 | ₹1 Cr | ₹10,000–13,000 |

| 40 | ₹1 Cr | ₹15,000+ |

Earlier you buy = Cheaper premium.

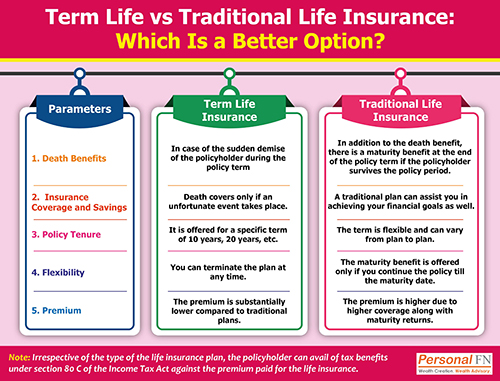

Term Insurance vs LIC Endowment Plans

Many Indians buy traditional policies from:

👉 Life Insurance Corporation of India (LIC)

Let’s compare.

| Feature | Term Plan | Endowment/Traditional |

|---|---|---|

| Purpose | Protection | Saving + Insurance |

| Return | No | Low |

| Premium | Low | High |

| Cover | High | Low |

👉 For protection, term plan is best.

Tax Benefits of Term Insurance

Term insurance gives tax benefits.

1️⃣ Premium Deduction (80C)

Up to ₹1.5 lakh per year.

2️⃣ Claim Amount (10D)

Death benefit is fully tax-free.

So:

✔ Save tax

✔ Protect family

👉 Related Read:

Internal Link: Mutual Fund Taxation in India

https://marketmeterab.blogspot.com/mutual-fund-taxation-india

Term Insurance and Loans

If you have:

Home loan

Car loan

Business loan

You must have term insurance.

Why?

👉 Your family should not carry your loan.

You can also take decreasing cover for loans.

Online vs Offline Term Insurance

| Feature | Online | Agent |

|---|---|---|

| Cost | Lower | Higher |

| Transparency | High | Medium |

| Convenience | High | Medium |

| Support | Online | Personal |

Most young Indians prefer online.

Common Mistakes Indians Make

Buying low cover

Hiding medical history

Choosing wrong nominee

Not reviewing policy

Mixing insurance with investment

Avoid these mistakes.

How to Buy Term Insurance (Simple Steps)

1️⃣ Compare plans online

2️⃣ Choose right cover

3️⃣ Fill details honestly

4️⃣ Do medical test (if asked)

5️⃣ Pay premium

6️⃣ Get policy document

Takes 30–60 minutes online.

Term Insurance + Investment = Best Strategy

Smart Indians do this:

| Tool | Purpose |

|---|---|

| Term Plan | Protection |

| SIP | Wealth |

| PPF | Safety |

| NPS | Retirement |

Example:

Term: ₹1 Cr

SIP: ₹3,000/month

PPF: ₹50,000/year

Balanced planning.

👉 Related Read:

Internal Link: Best SIP Amount for Beginners

https://marketmeterab.blogspot.com/best-sip-amount-india

Term Insurance vs Health Insurance

| Feature | Term | Health |

|---|---|---|

| Covers | Death | Hospital Bills |

| Beneficiary | Family | Policyholder |

| Purpose | Income Replacement | Medical Protection |

👉 You need both.

Nomination and Claim Process

Always:

✔ Add correct nominee

✔ Update after marriage

✔ Inform family about policy

Claim process:

1️⃣ Inform company

2️⃣ Submit death certificate

3️⃣ Provide documents

4️⃣ Receive payout

Good companies settle in 15–30 days.

Safety of Term Insurance

Because it is regulated by IRDAI:

✔ No fraud companies

✔ Clear rules

✔ Customer grievance system

So, it is reliable.

Statutory Disclaimer

Insurance is subject to terms and conditions of the policy document. Premiums, benefits, and rules may change as per regulations. This article is for educational purposes only and does not constitute professional financial advice. Readers should evaluate their personal needs and consult certified advisors before purchasing any insurance product. All insurers are regulated by the Insurance Regulatory and Development Authority of India.

Frequently Asked Questions (FAQ)

Q1. Is term insurance compulsory?

No, but highly recommended.

Q2. What if I stop paying premium?

Policy may lapse. Protection ends.

Q3. Can I increase cover later?

Some plans allow. Better buy enough early.

Q4. Is medical test necessary?

For high cover, yes.

Q5. Can housewives buy term plan?

Yes, if eligible and income criteria met.

Useful Video & Image Resources

Term Insurance Explained (Hindi):

https://www.youtube.com/watch?v=F8M2Q9L7X4AHow to Choose Best Term Plan:

https://www.youtube.com/watch?v=K9F3L2M8X7QIRDAI Official Website:

https://www.irdai.gov.inLIC Term Plans Page:

https://licindia.in

Bibliography

IRDAI Consumer Guidelines

Insurance Act of India

LIC & Private Insurer Brochures

Income Tax Act – Section 80C & 10D

RBI Financial Literacy Reports

Suggested Internal Links for MarketMeterAB

Long Term vs Short Term Investing

https://marketmeterab.blogspot.com/long-term-vs-short-term-investingHow Dividends Work in India

https://marketmeterab.blogspot.com/how-dividends-workNPS Scheme in India Explained

https://marketmeterab.blogspot.com/nps-scheme-indiaEPF vs PPF Difference Explained

https://marketmeterab.blogspot.com/epf-vs-ppf-differenceCharges in Stock Trading Explained

https://marketmeterab.blogspot.com/stock-trading-charges-india

Final Words

Term insurance is not about profit.

It is about:

✅ Responsibility

✅ Love for family

✅ Financial discipline

✅ Peace of mind

If you earn today, your family depends on you.

👉 A small premium today can protect their entire future.

Remember: First insure, then invest. Always.

Comments

Post a Comment