Child Education Planning in India: A Practical Guide for Parents to Secure Their Child’s Future

Child Education Planning in India: A Practical Guide for Parents to Secure Their Child’s Future

SEO Title

Child Education Planning in India: Smart Financial Guide for Parents (2026)

Meta Description

Learn how to plan child education expenses in India with smart investment strategies, SIP, Sukanya Samriddhi Yojana, and education funds. A practical guide for Indian parents.

Introduction

Every parent in India dreams of giving their child the best possible education. Whether it is engineering, medicine, management, or studying abroad, quality education can open doors to a bright future.

However, the cost of education is rising rapidly. For example:

Engineering degree today: ₹8–20 lakh

Medical education: ₹50 lakh – ₹1 crore

Studying abroad: ₹50 lakh – ₹1.5 crore

If parents do not plan early, arranging such a large amount later can become financially stressful.

This is why child education planning is essential. It allows parents to build a dedicated fund over time so their child’s dreams are not limited by financial constraints.

This guide explains:

How much money to save

Practical examples for Indian families

Why Child Education Planning Is Important

Education costs in India have increased dramatically in the last two decades.

Here are some important reasons why planning is necessary.

Rising Education Inflation

Education inflation in India is around 10–12% per year, which is higher than normal inflation.

Limited Education Loans

Education loans help but may create financial pressure later.

Early Planning Reduces Stress

If investments start early, parents can accumulate the required funds gradually.

Financial Security

A well-planned education fund ensures that the child’s future is secure regardless of financial circumstances.

Step 1: Estimate Future Education Cost

The first step in education planning is estimating how much money will be required in the future.

Example:

Suppose the current cost of an engineering degree is ₹15 lakh.

If education inflation is 10%, the cost after 15 years becomes:

Future Cost = Present Cost × (1 + Inflation)^Years

Calculation:

₹15,00,000 × (1.10)^15 ≈ ₹62 lakh

So parents may need around ₹60–65 lakh for engineering education after 15 years.

Step 2: Set a Target Education Fund

Once you know the estimated cost, you can decide the target amount.

Example target corpus:

| Education Goal | Estimated Future Cost |

|---|---|

| Engineering in India | ₹50–70 lakh |

| Medical education | ₹80 lakh – ₹1.5 crore |

| MBA in India | ₹30–50 lakh |

| Studying abroad | ₹70 lakh – ₹1.5 crore |

This helps create a clear financial goal.

Step 3: Start Investing Early

Time is the most powerful factor in wealth creation.

If parents start investing when the child is young, compounding works effectively.

Example:

| Child Age | Monthly Investment | Value After 18 Years |

|---|---|---|

| 1 year | ₹5,000 | ₹40–45 lakh |

| 5 years | ₹5,000 | ₹25–30 lakh |

| 10 years | ₹5,000 | ₹12–15 lakh |

Assuming average 12% annual return.

Starting early significantly reduces the investment burden.

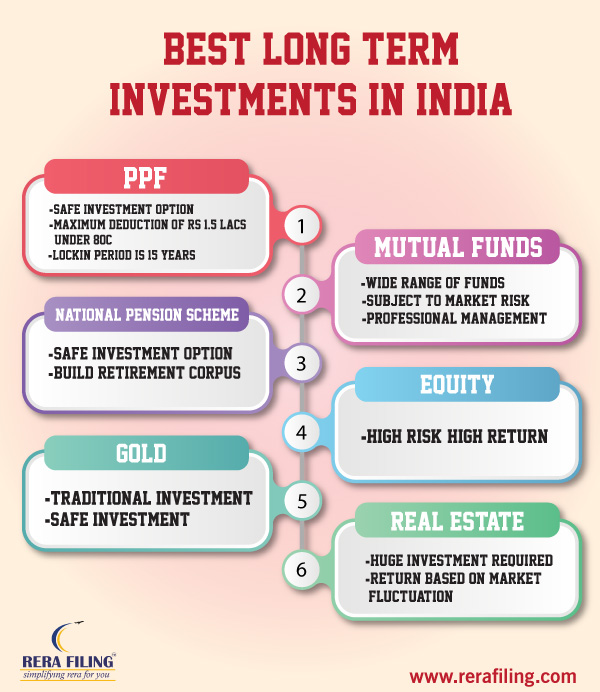

Best Investment Options for Child Education in India

1. Mutual Fund SIP

Systematic Investment Plans (SIP) in equity mutual funds are one of the best tools for long-term education planning.

Benefits:

Higher return potential

Flexible investment

Expected return: 10–12% over long term

2. Sukanya Samriddhi Yojana (SSY)

This scheme is specifically designed for the girl child.

Features:

Government-backed scheme

Attractive interest rate

Tax benefits under Section 80C

It is ideal for saving for a daughter’s education.

3. Public Provident Fund (PPF)

PPF is a safe long-term investment option.

Benefits:

Government guarantee

Tax-free returns

15-year investment period

4. Child Insurance Plans

Some insurance companies offer child education plans combining insurance and savings.

However, returns may be lower than mutual funds.

5. Fixed Deposits for Short-Term Goals

FDs can be useful for short-term education goals but may not beat inflation over long periods.

Example: Education Planning for Indian Parents

Let us consider a practical example.

Anita and Raj have a 2-year-old son.

They expect higher education costs of about ₹50 lakh after 16 years.

If they invest through mutual fund SIP with 12% annual return, the required monthly investment is:

Monthly SIP ≈ ₹8,500

This systematic approach can help them achieve the target comfortably.

Child Education Planning Chart

Child Birth

↓

Start Investments Early

↓

Regular Monthly SIP

↓

Compounding Growth

↓

Education Corpus Ready

This simple cycle helps parents prepare financially.

Common Mistakes Parents Should Avoid

Delaying Investments

Starting late requires higher monthly investments.

Ignoring Education Inflation

Education costs increase faster than normal inflation.

Overdependence on Education Loans

Loans can create long-term financial pressure for children.

Not Diversifying Investments

A mix of equity and safe investments works best.

Internal Resources on MarketMeterAB

Readers interested in financial planning may also explore related articles on the blog:

These topics help families build long-term financial security.

Educational Video Resource

Helpful explanation on child education planning:

https://www.youtube.com/watch?v=Fh6Y8tQ2x0Q

FAQ: Child Education Planning in India

When should parents start planning for child education?

Ideally immediately after the child is born. Early investments provide maximum compounding benefit.

How much money is required for higher education in India?

Depending on the field, higher education may cost ₹30 lakh to ₹1.5 crore in the future.

Are mutual funds good for child education planning?

Yes. Equity mutual funds through SIP help generate higher returns and beat inflation over long periods.

What is the best scheme for a girl child’s education?

Sukanya Samriddhi Yojana is one of the best government schemes for girl child education savings.

Statutory Disclaimer

This article is for informational and educational purposes only. It does not constitute financial or investment advice. Readers should consult a qualified financial advisor before making investment decisions.

Bibliography

Reserve Bank of India – Financial Education Resources

Securities and Exchange Board of India (SEBI) Investor Awareness Material

Ministry of Finance, Government of India – Savings Schemes Information

National Institute of Public Finance and Policy – Education Cost Studies

Final Thoughts

Child education planning is not only about money — it is about giving your child the freedom to pursue their dreams without financial limitations.

By estimating future costs, starting investments early, and choosing the right financial instruments, parents in India can build a strong education fund.

The key rule is simple:

Start early, invest regularly, and stay disciplined.

Over time, small investments can grow into a large fund that supports your child’s bright future.

Comments

Post a Comment