Retirement Corpus Calculation in India: How Much Money Do You Need to Retire Comfortably

Retirement Corpus Calculation in India: How Much Money Do You Need to Retire Comfortably

Description

Learn how to calculate retirement corpus in India with simple formulas, examples, and investment strategies. A practical guide for Indian citizens to plan retirement effectively.

Introduction

One of the biggest questions people ask while planning retirement is simple:

“How much money will I need after retirement?”

This amount is called the retirement corpus — the total savings required to live comfortably after you stop working.

Many Indians underestimate this number because they forget two key factors:

If retirement planning is done properly, your investments can generate enough income to support your lifestyle without financial stress.

In this guide, we will explain in a simple practical way:

What retirement corpus means

Step-by-step calculation method

Practical Indian examples

Tools and strategies to build this corpus

What is Retirement Corpus?

Retirement corpus simply means:

The total amount of money required at retirement to cover all future expenses for the rest of life.

This corpus should cover:

Monthly living expenses

Healthcare expenses

Lifestyle expenses

Emergency funds

For most middle-class Indian families, the retirement corpus usually ranges between:

₹1.5 Crore – ₹5 Crore, depending on lifestyle and inflation.

Why Retirement Corpus Calculation is Important

Proper calculation helps you:

1. Avoid Financial Stress

Without proper planning, retirement may become financially difficult.

2. Maintain Lifestyle

You can continue the same standard of living even after retirement.

3. Beat Inflation

Prices rise over time, so future expenses must be estimated carefully.

4. Build Systematic Investments

Once the target corpus is known, investment planning becomes easier.

Key Factors That Affect Retirement Corpus

Before calculating the corpus, consider these factors.

Current Age

The younger you start, the easier it is to build a large corpus through compounding.

Retirement Age

Most Indians retire around 60 years.

Monthly Expenses

Your current spending determines future retirement needs.

Inflation Rate

In India, long-term inflation generally averages around 5–7%.

Life Expectancy

Retirement planning should consider 80–85 years of life expectancy.

Step-by-Step Retirement Corpus Calculation

Let us understand the calculation with a simple method.

Step 1: Estimate Current Monthly Expenses

Suppose your current monthly expense is:

₹50,000 per month

Annual expense:

₹50,000 × 12 = ₹6,00,000

Step 2: Adjust for Inflation

Assume:

Inflation rate = 6%

Years to retirement = 25

Future expense formula:

Future Expense = Current Expense × (1 + Inflation)^Years

Example calculation:

₹50,000 × (1.06)^25 ≈ ₹2,15,000 per month

So your future monthly expense at retirement = ₹2.15 lakh.

Step 3: Calculate Annual Retirement Expense

₹2,15,000 × 12 = ₹25,80,000 per year

Step 4: Apply Retirement Corpus Rule

Financial planners often use the 25X rule.

Retirement Corpus = Annual Expense × 25

Calculation:

₹25,80,000 × 25 ≈ ₹6.45 Crore

So in this example, the required retirement corpus is approximately:

₹6–6.5 Crore

Retirement Corpus Calculation Chart

Current Monthly Expense → Inflation Adjustment → Future Expense

↓

Annual Expense

↓

Multiply by 25 (Rule)

↓

Retirement Corpus

This is the simplified retirement planning model used by many financial planners.

Practical Example for Indian Middle-Class Family

Rahul is a 32-year-old professional in Pune.

Details:

| Parameter | Value |

|---|---|

| Current age | 32 |

| Retirement age | 60 |

| Monthly expense | ₹60,000 |

| Inflation | 6% |

| Years to retirement | 28 |

Estimated retirement expense:

₹3 lakh per month

Annual expense:

₹36 lakh

Required retirement corpus:

₹36 lakh × 25 = ₹9 Crore

So Rahul should aim for ₹8–9 crore retirement corpus.

Investment Options to Build Retirement Corpus

To build a large retirement corpus, Indians should diversify investments.

1. Mutual Fund SIP

Equity mutual funds are powerful for long-term growth.

Expected return: 10–12%

Best suited for long-term investors.

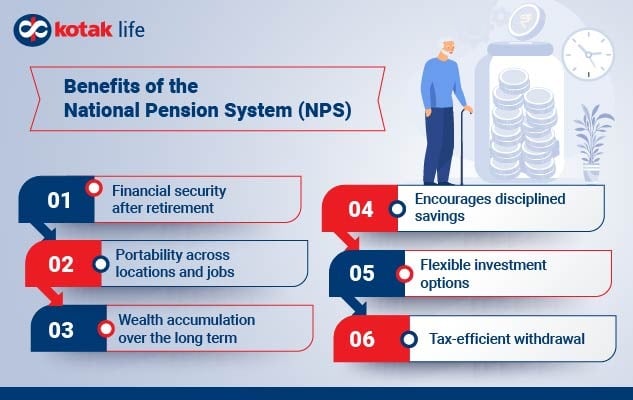

2. National Pension System (NPS)

NPS is designed specifically for retirement.

Benefits:

Tax deduction under Section 80CCD(1B)

Market-linked returns

Pension income after retirement

3. Employee Provident Fund (EPF)

EPF helps salaried employees automatically accumulate retirement savings.

Government backed and relatively safe.

4. Public Provident Fund (PPF)

PPF provides:

Tax-free returns

Long-term compounding

Government guarantee

5. Hybrid Mutual Funds

Balanced funds combine:

Equity growth

Debt stability

They are useful for people approaching retirement.

Monthly Investment Needed for Retirement

Here is an example of monthly investment required.

| Age | Monthly SIP | Estimated Corpus at 60 |

|---|---|---|

| 25 | ₹8,000 | ₹4 Crore |

| 30 | ₹12,000 | ₹4 Crore |

| 35 | ₹22,000 | ₹4 Crore |

| 40 | ₹40,000 | ₹4 Crore |

Starting early reduces investment pressure significantly.

Common Retirement Planning Mistakes

Avoid these common errors.

Ignoring Inflation

Inflation is the biggest enemy of retirement savings.

Starting Too Late

Many people begin retirement planning after 40.

Overdependence on Fixed Deposits

FD returns often fail to beat inflation.

Not Reviewing Investments

Investment portfolios should be reviewed every year.

Internal Resources on MarketMeterAB

For more financial knowledge, readers may also explore:

These articles help Indian investors build strong financial foundations.

Helpful Educational Video

Understanding retirement planning visually:

https://www.youtube.com/watch?v=2R7S7Fh1cWk

Frequently Asked Questions (FAQ)

How much retirement corpus is enough in India?

Most middle-class families require ₹3–10 crore depending on lifestyle, inflation, and location.

What is the 25X rule in retirement planning?

The rule suggests that retirement corpus should be 25 times annual expenses.

What is a safe withdrawal rate after retirement?

Financial planners often suggest 3–4% annual withdrawal to sustain funds for 25–30 years.

Should Indians invest in mutual funds for retirement?

Yes. Equity mutual funds help generate higher returns and beat inflation over long periods.

Statutory Disclaimer

This article is for informational and educational purposes only. It does not constitute financial or investment advice. Readers should consult a certified financial advisor before making investment decisions.

Bibliography

Reserve Bank of India – Financial Literacy Materials

Securities and Exchange Board of India (SEBI) Investor Awareness Guide

National Pension System Trust – Official Resources

Ministry of Finance, Government of India – Pension Schemes

Final Thoughts

Retirement planning is not about guessing numbers — it is about calculating realistically and investing consistently.

If you understand your future expenses, adjust them for inflation, and invest wisely, building a retirement corpus becomes achievable.

The most important step is simple:

Start early, stay disciplined, and allow compounding to build your financial future.

Comments

Post a Comment